Understanding deductibles is one of those finance-and-health crossroads that suddenly matters the day you get a big medical bill. In plain terms, a deductible is the amount you pay out of pocket for covered care before your insurer starts to share the cost. That sounds simple, but choices you make when picking a plan — monthly premium, whether you want an HSA, and how much risk you’re willing to carry — all change how that deductible feels in real life. Take Maya, a mid-30s graphic designer who lives in a metro area and switches jobs in 2025: she compared quotes on tools like PolicyWise and DeductibleDirect, debated a low-premium high-deductible plan versus a pricier low-deductible alternative, and used projections to see which option kept her monthly budget steady while protecting against a hospital stay. This article walks through what a deductible actually does, how it interacts with copays, coinsurance and out-of-pocket maximums, and practical moves you can use to avoid surprises. Expect clear examples, a few short case studies with Maya, and pointers to resources and services — from ClaimSmart to CoverageClarity — that help you pick the best plan for your situation.

In brief — what matters most

Deductible vs premium: a lower monthly premium usually means a higher deductible.

High-deductible plans: often paired with an HSA for tax-advantaged savings.

Family vs individual: family deductibles pool costs differently than single plans.

After the deductible: you may still pay coinsurance or copays until the out-of-pocket maximum is reached.

Tools and tips: services like PremiumPath and RiskReveal can help forecast costs and compare scenarios.

How a deductible works and why it’s not the same as a premium

Start with the basics: a deductible is what you must pay for covered services before your insurer contributes. A premium is the recurring charge you pay to keep the policy active. They’re linked — insurers trade off between the two to price plans.

In Maya’s case, a plan with a $2,500 deductible meant she paid less each month but would cover the first big emergency herself. She ran a quick scenario using a calculator on InsureInsight to see how often she’d cross that threshold based on projected visits and prescriptions. The result helped her decide whether to accept more monthly cost for lower out-of-pocket risk.

Key takeaway: your deductible is an annual threshold that resets on your plan year, and choosing it is a trade-off between monthly budget and immediate risk exposure.

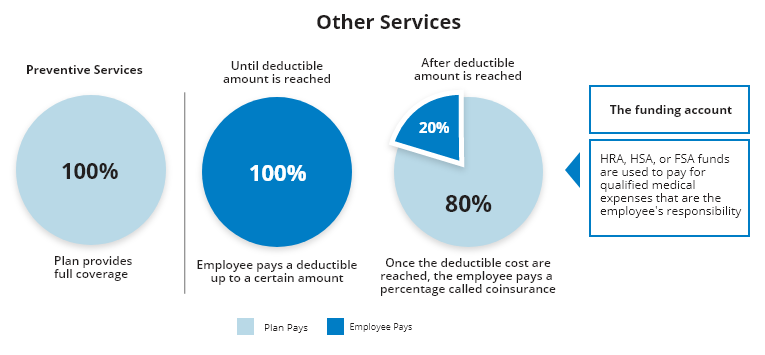

Coinsurance, copays and out-of-pocket maximums — the fine print that matters

Once you hit the deductible, most plans shift you into coinsurance: a percentage of the bill you still owe. Typical coinsurance sits between 20% and 40%, though networks and plan tiers change that rate. Copays are fixed fees and often don’t count toward the deductible.

Don’t forget the out-of-pocket maximum — the ceiling on what you’ll pay in a year. The Affordable Care Act kept limits for marketplace plans, which means catastrophic loss protection exists, but non-market policies can differ. Maya used resources from an insurance beginner’s guide to check those limits and avoid surprise exposure.

Key sentence: understand coinsurance and copays as the second act after the deductible — they determine how much you still pay on recurring or big claims.

Which deductible fits your life: scenarios and a simple decision method

People pick plans for different reasons. If you’re healthy with few planned visits, a high-deductible plan plus an HSA can be economical. If you expect frequent care — chronic conditions, pregnancy, or a large family — a low-deductible plan usually saves money overall despite higher premiums.

Maya mapped three scenarios: a quiet year, a year with several specialist visits, and a year with hospitalization. She fed expected costs into a comparison tool on PolicyWise and bookmarked tips from a health insurance tips resource to decide. The result: she selected a mid-tier plan that balanced premium and deductible and opened an HSA for emergencies.

Key sentence: choosing a deductible is about matching predicted healthcare usage to financial tolerance — run scenario tests before you decide.

Family vs individual deductibles and high-deductible health plans (HDHPs)

Individual deductibles apply per person, while family deductibles often let the whole household pool payments so the plan starts paying once the family threshold is met. That can speed up protection for large families but may not help a single member with heavy costs until the family total is reached.

HDHPs often pair with HSAs, making them attractive as tax-smart savings vehicles in 2025. Services like DeductibleDirect and ClaimSmart now integrate HSA projections so users can see tax and cashflow impacts in one view.

Key sentence: for families, compare how quickly a family deductible is met versus individual limits to know when coverage will kick in.

Practical moves to manage deductibles and avoid surprises

Start by building a short emergency buffer earmarked for medical bills. If you choose an HDHP, open an HSA and contribute consistently — the tax benefits in many jurisdictions still make this worthwhile in 2025. You can also negotiate bills, ask about payment plans, and confirm whether services are in-network to reduce coinsurance.

Use modern comparison and claims tools — for instance, Maya used PremiumPath to project premium-versus-deductible outcomes and RiskReveal to model worst-case scenarios. When she had a billing question, she followed the step-by-step advice from a page on how to file an insurance claim and relied on practical guidance from right insurance tips to dispute errors. For quick policy term clarifications she consulted a guide to explain common policy terms.

Key sentence: combine budgeting, HSAs, proactive in-network use and digital tools like CoverageClarity and InsureInsight to keep deductible risk manageable and predictable.

Final practical example: how a $2,000 deductible played out

Scenario: Maya had a $2,000 deductible, 20% coinsurance, and a $6,000 out-of-pocket max. A broken wrist led to $4,500 in covered charges. She paid $2,000 (deductible) + 20% of the remaining $2,500 ($500) = $2,500 total out-of-pocket, then the insurer covered the rest until her out-of-pocket max was reached.

She tracked the claim with ClaimSmart and verified coverage using advice from auto insurance coverage benefits resources for cross-checking billing practices. That practical tracking saved her several hundred dollars in coding errors and ensured the claim applied correctly to her deductible.

Key sentence: a clear, step-by-step claim and billing review can materially reduce what counts toward your deductible and save real money.

How brands and tools can help you compare plans

Insurers and insurtechs now provide side-by-side comparisons that simulate your year based on diagnosis codes, typical visit counts, and prescriptions. Companies like SafeSure and platforms labeled BenefitBasics offer quick scenario builders, while services such as PolicyWise and DeductibleDirect focus on deductible-specific forecasting.

When you shop in 2025, look for tools that calculate not just premiums but expected annual out-of-pocket totals, including coinsurance and copays. That’s how Maya avoided a plan that looked cheap monthly but cost more in typical-use scenarios. Use the resources linked here to deepen your review before signing up.

Key sentence: rely on scenario-driven comparison tools to move beyond sticker premiums and see the real annual cost picture.