When you’re shopping for coverage, the first stop is usually a stack of quotes — but those numbers alone don’t tell the whole story. In this piece we follow Alex, a mid-30s freelance photographer, as they hunt for a smarter policy in 2025. Alex learns fast that an appealing premium can hide weak limits, surprise exclusions, or a sky-high deductible that makes a low price essentially meaningless. By comparing details side‑by‑side — not just the price — Alex uncovers real differences: one quote includes roadside assistance and rental-car reimbursement, another has strong liability limits but a confusing claims process. Along the way Alex experiments with comparison tools like SmartQuote and InsureCompare, and runs sample scenarios to see how each policy responds to a real-world claim. This article shows the practical checks that turn raw quotes into confident choices: how to read limits and exclusions, where discounts commonly hide, why insurer reputation matters, and which online features speed up decisions. Expect concrete examples, a few cautionary tales from Alex’s searches, embedded videos with quick walkthroughs, and direct resources to dig deeper on specific topics. By the end you’ll know how to compare like a pro and pick coverage that actually protects what matters.

En bref — key takeaways

Compare features first: a lower premium isn’t helpful if limits or coverages are missing.

Watch out for out-of-pocket costs: check deductibles, copays and hidden fees before choosing.

Use tech wisely: platforms such as QuoteWise or QuoteNavigator speed comparisons but verify each line item manually.

Reputation matters: claims handling and customer service often trump a few dollars saved on premiums.

Customize coverage: tailor options like endorsements or riders rather than buying one-size-fits-all policies.

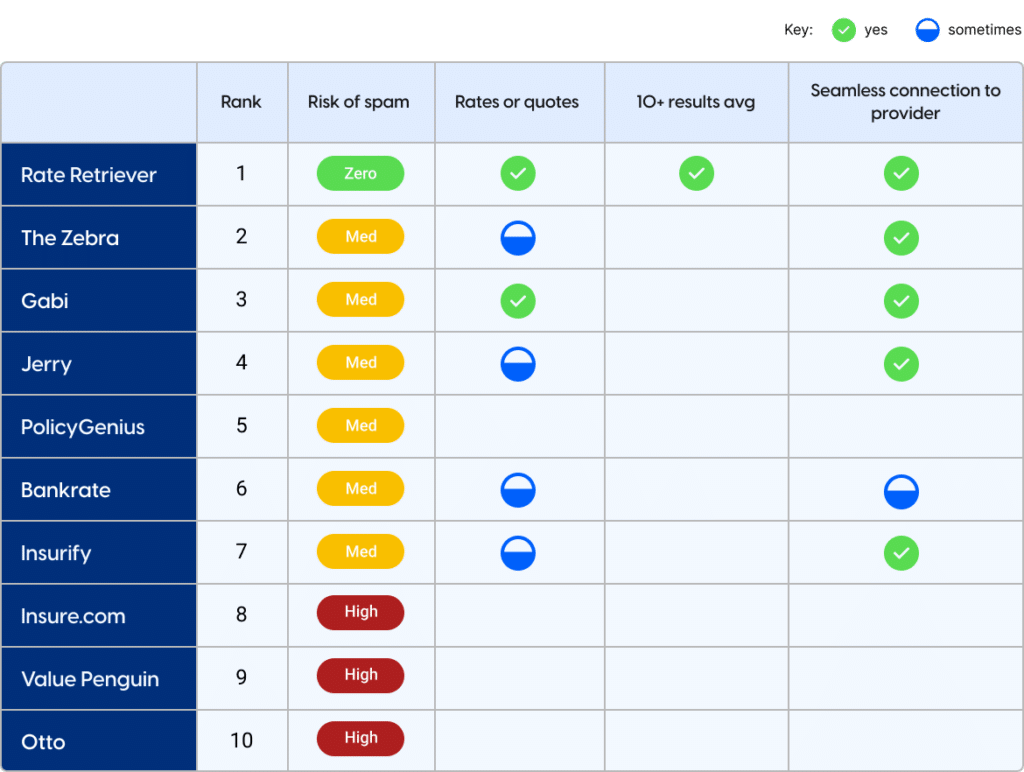

How to compare insurance quotes effectively in 2025

Start by treating each quote as a mini contract, not just a number. That means scanning for coverage limits, definitions of covered events, and any specific exclusions that could leave you exposed.

Alex found that one insurer offered a tempting premium but excluded flood-related damage for equipment — a dealbreaker for a photographer who works on riverside shoots. Always cross-check those exclusions and ask for the exact policy wording when anything looks unclear. This practice prevents surprises during a claim and saves time in the long run.

Focus on coverage details before price

When Alex compared two auto quotes, the cheaper option had a lower premium but a substantially higher deductible and narrower collision coverage. That meant a small accident would still cost them hundreds out of pocket.

To better understand premium drivers, Alex read a guide on what affects insurance premiums, then ran scenarios to see how different deductibles changed annual costs. This exercise revealed that opting for a slightly higher premium with lower deductible actually reduced expected annual expenses given Alex’s driving habits. Clear evaluation of these trade-offs saves money and grief later.

Insight: comparing the fine print first reveals the true value behind any quoted price.

Key quote factors: limits, exclusions, and deductibles explained

Not all limits are equal. Liability caps, per‑incident maximums, and aggregate limits can change how much an insurer will pay across multiple claims. Alex once assumed a policy’s « $100,000 limit » covered everything — only to discover it applied per person, not per accident.

Understanding deductibles is equally crucial. A detailed explainer helped Alex weigh choosing a lower deductible versus saving on the monthly premium; more background is available in this deductible guide. For policy language and common clauses, consult an overview like how insurance policies work to decode terms that insurers often bury in fine print.

Insight: precise definitions change outcomes — always confirm whether limits are per incident or aggregate and how deductibles apply.

Exclusions that matter — real examples

Alex discovered an exclusion clause for equipment used commercially in a homeowners policy that seemed to cover personal gear. Because of that, they secured a targeted rider instead of assuming coverage. For renters who want clarity on personal property, checking a specialized resource like renters coverage basics avoids similar surprises.

Small clauses can cost thousands during a claim. Asking an agent to point out exclusions and requesting written confirmation of any verbal assurances closed the loop for Alex and prevented future disputes. Insisting on those confirmations is a simple habit that pays off.

Insight: never assume coverage — get exclusions spelled out in writing before you buy.

Beyond the quote: insurer reputation, claims handling and real-world testing

Price and coverage are only part of the equation. Alex prioritized carriers with strong claims satisfaction and a straightforward digital claims process. That research included reading reviews, checking complaint ratios, and testing each insurer’s mobile app for filing a mock claim.

Platforms such as SmartCover and InsureInsight allowed side‑by‑side customer service metrics, while brokers using PolicyScout and QuoteMaster helped explain subtle policy differences. Real-world testing — like timing how long an adjuster took to respond to a sample query — gave Alex confidence that the chosen insurer would act quickly when needed.

Insight: efficient claims handling and transparent communication often matter more than shaving off a small amount from the premium.

When a cheap policy becomes expensive

Alex once bought the lowest-cost auto policy recommended by a low‑price aggregator, only to experience long delays when a minor accident occurred. The slow claims response and confusing paperwork cost far more in stress and replacement rentals than the monthly savings ever delivered.

A better route was using a tool like QuoteNavigator to shortlist options, then verifying responsiveness through reviews and test calls. Combining tech tools with basic human checks made the final pick both affordable and resilient.

Insight: speed and clarity in claims processes protect your money and peace of mind.

Practical steps to compare quotes like a pro

First, gather standardized quotes: request the same coverages, limits and deductibles from each insurer so comparisons are apples‑to‑apples. Alex created a one-page checklist of required coverages and used it when speaking with agents to ensure consistency.

Second, leverage specialized resources: when tailoring coverage for specific needs Alex consulted a guide on customizing coverage and checked options for pet protection via pet insurance explained. For homeowners or renters, articles like home insurance protection helped identify must-have endorsements.

Third, simulate claims: ask each insurer how a claim of $X would be handled, and which coverages apply. These mini-scenarios unearthed differences that numbers alone missed. Alex’s practice of running three likely claim scenarios turned indecision into actionable comparison points quickly.

Insight: structured comparisons and scenario testing reveal how policies behave when it matters most.

Tools and platforms worth trying

Comparison engines and broker tools accelerate the process, but they aren’t a substitute for reading the policy. Try multiple sources: an aggregator for breadth, a direct carrier site for policy wording, and a local agent for personalized advice. Names Alex tested included QuoteWise and PolicyMatcher, and each offered different strengths — speed versus detail.

Finally, save your favorite quotes and revisit them after 24 hours; a little distance often highlights missing elements or reveals better options. This pause helped Alex avoid impulse purchases and choose coverage that balanced price and protection effectively.

Insight: mix automated comparison tools with human checks for the best result.

For deeper reading on related topics, check expert resources on life coverage basics at life insurance fundamentals and on balancing income risks via disability protection. These guides complement the comparison tactics covered here and help build a long-term protection plan.