Navigating insurance can feel like stepping into a thick forest without a trail — policies use niche language, coverage limits hide surprises, and people often only look at their documents when something goes wrong. In this guide I follow Alex, a thirty-something renter who just bought a used car and is trying to understand what coverage actually protects them. Together we unpack the essentials: what an insurance contract does, which parts of a policy to read first, and how to spot costly gaps before a claim. You’ll see practical examples — like why a homeowner’s policy rarely covers flood damage unless you buy a separate product, or how a low deductible can make sense for frequent claims — and get pointers on modern tools and insurers that streamline shopping and claims in 2025. Along the way we reference comparison platforms and tech-first carriers to help you make decisions faster. By the end you’ll know how to compare offers, read the fine print, and take simple steps to make sure you and your family aren’t caught short when the unexpected happens. This knowledge turns insurance from a mystery into a tool for real protection.

En bref — key takeaways you should remember now: know your premium and deductible; confirm your coverage limits match your assets; check the exclusions (floods, wear-and-tear, intentional damage); use comparison tools to shop smarter; update beneficiaries and property values after life changes. These moves reduce nasty surprises during a claim and make your coverage actually useful.

Understanding insurance basics: what coverage actually means

At its heart, insurance is a contract: you pay a premium, the insurer accepts certain risks, and the policy spells out when money will be paid. Alex learned this the hard way after assuming “comprehensive” auto coverage would replace a phone stolen from their unlocked car — it didn’t, because the policy listed theft specifics under exclusions.

Think of the policy as a rulebook: the declarations page gives the headline facts — policyholder name, coverage types, limits, and period — while the detailed sections explain conditions and exclusions. Knowing where to look saves time and stress when you need to file a claim. Always start with the declarations page and the “what we cover” section; they answer the biggest practical questions. This clarity makes the policy manageable instead of overwhelming.

How an insurance policy works: premiums, deductibles, and limits

Three terms decide most outcomes: the premium (what you pay), the deductible (what you pay first when you claim), and the coverage limit (the maximum the insurer will pay). For example, a $500 deductible means you pay the first $500 of a covered loss; if the repair is $4,500 and the limit is $10,000, the insurer pays $4,000 after your deductible.

Alex chose a lower deductible after a minor accident last year because the peace of mind outweighed the slightly higher monthly cost. That trade-off — higher premium for lower out-of-pocket risk — is personal and depends on savings, risk tolerance, and how often you expect to file. Always run the math for at least two scenarios before picking levels. Understanding those trade-offs helps you select coverage that actually fits your finances.

Common coverage types explained: health, auto, home, life, disability, and travel

Policies come in many flavors and each serves a different need. Health insurance handles medical costs — providers like Oscar Health have focused on tech-forward care and member tools. Auto insurance covers collision, property damage, and liability; new entrants like Root Insurance and Metromile emphasize telematics and pay-per-mile models that may lower costs for low-mileage drivers. Homeowners (and renters) protect dwellings and belongings; companies such as Hippo often add smart-home discounts. Life insurance provides a death benefit; agents and aggregators like Policygenius help shoppers compare options. Disability replaces income if you can’t work, and travel covers common trip mishaps abroad.

Insurers and platforms differ in pricing, user experience, and how they handle claims. Tech-forward names like Lemonade, Gabi, and ClearCover aim for fast quotes and simple apps, while brokers such as CoverHound and Policygenius aggregate many carriers so you can compare. Picking the right provider can be as important as picking the right coverages.

Riders, endorsements, and exclusions: what to watch for

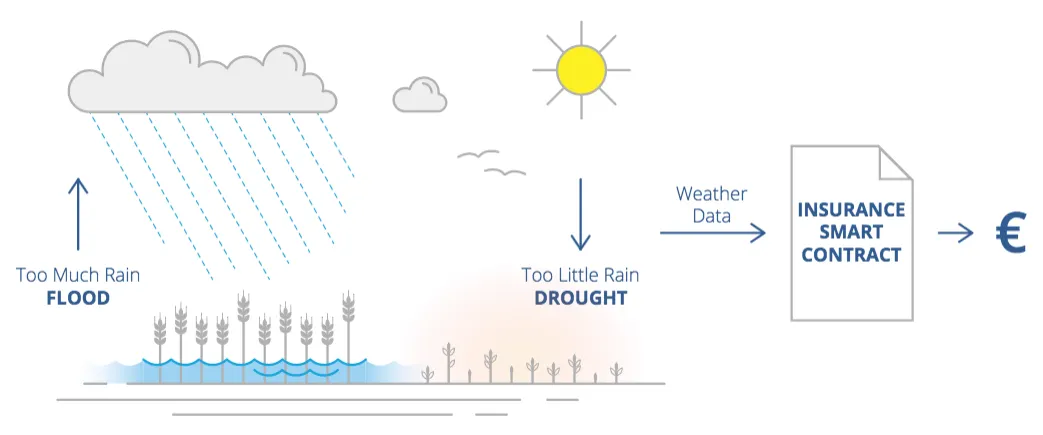

Small lines can have big consequences. Exclusions tell you what’s not covered — for instance, standard homeowners policies often exclude flood and earthquake damage. That’s why Alex added a flood rider after moving into a floodplain-susceptible area. Endorsements (or riders) modify your baseline coverage: they can add protection for high-value jewelry or reduce coverage in exchange for lower premiums.

Before you sign, search for vague language like “reasonable” or “customary,” and ask for examples. If a term is unclear, get it clarified in writing. When you understand endorsements and exclusions, you avoid nasty denials later — a clear policy prevents surprise shortfalls at claim time. For a practical next step, schedule a free policy review to pinpoint gaps and possible endorsements that fit your situation.

How to compare policies and shop smart in 2025

Comparing policies is both art and science: you must match coverage levels, endorsements, and real-world service. Start by assessing your risks — car usage, home rebuild cost, health needs, or business liabilities. Then compare total cost over a year (premiums plus potential deductible exposure) rather than focusing on the lowest monthly price alone. Alex compared three carriers, including a telematics-based auto insurer and a traditional firm, and used savings estimates to pick the right balance.

Use technology but verify details. Aggregators and comparison tools like Policygenius, CoverHound, and services from Gabi speed up quote collection. Insurtech names such as ClearCover and Lemonade offer streamlined apps and fast claims, while industry specialists like Next Insurance focus on small-business needs. If you want side-by-side offers, compare quotes with a broker who can translate policy language into outcomes you understand.

Remember to check carrier financial strength and complaint ratios, not just price. A cheaper policy that denies valid claims isn’t a bargain. Smart shopping means balancing cost, coverage, and carrier reliability so your protection works when it matters most.

Filing claims: timing, documentation, and common denial reasons

A smooth claim is mostly paperwork and timing. Report losses promptly, photograph damage, keep receipts, and follow the insurer’s instructions for documentation. Common denial reasons include late filing, claiming for excluded causes, or exceeding coverage limits. Alex saw a claim delayed because they missed a required police report for a theft — a simple checklist would have prevented the delay.

Store policies and claim documents both digitally and physically. Update beneficiaries and property values after major life events like marriage or renovation. If a denial occurs, insist on a written explanation and ask for an appeal; many disputes resolve with clear documentation. Preparing your claim ahead of time reduces stress and speeds recovery when an incident happens.

Next steps: review, update, and ask for help

Set an annual reminder to review policies, especially after life changes: new home improvements, a new car, a new child, or a business pivot. Revisiting your declarations page and endorsements every year prevents unpleasant surprises. If you’re unsure where to start, get a tailored review from a trusted service — you can get a tailored quote or review your policy online to identify easy improvements.

When comparing, ask three direct questions to each prospective insurer: what’s covered, what’s excluded, and how do you handle claims? Use tools and brokers to save time: try learn more about coverage options or request a policy review to get personalized recommendations. Taking these steps turns insurance from a confusing contract into a clear safety net you can rely on.