Pet insurance explained: giving your pet the best care looks at why more owners view coverage as essential, how policies actually work, and what to check before you sign. Veterinary care has become more advanced — and more expensive — so decisions once made on the fly now have real financial consequences. Meet Sam, a graphic designer in Boston, and his labrador Luna: when Luna swallowed a toy in 2024, an emergency surgery cost nearly $4,500 and changed how Sam budgets for pet care. This piece walks through the mechanics of pet insurance, the typical promises and fine print, and practical scenarios — from puppies to senior cats to exotic companions — showing when insurance saves money, and when a savings account might do. You’ll also find tangible tips for picking a plan that fits your lifestyle, and ways to compare pet cover alongside other household protections. Expect clear comparisons of coverage types like accidents, illness, and wellness, real-world cost cues, and a short roadmap to file claims fast so you can focus on your animal, not the paperwork.

En bref: Coverage typically includes emergencies, diagnostics, meds, and surgery; costs depend on species, breed, age and location; wellness add-ons cover vaccines and dental; pre-existing conditions are usually excluded; compare multiple providers and read waiting periods carefully. These points help you decide whether to buy a plan or build a buffer fund.

How pet insurance works: a simple breakdown to help you decide

Pet insurance functions much like human health insurance: you pay a regular premium, cover an optional deductible and copay, then submit claims for reimbursement after your vet visit. Most providers require you to pay the vet up front and then file for reimbursement, so keeping detailed receipts matters.

Typical steps are: visit a licensed vet, pay the bill, submit a claim (photo or upload), and get reimbursed by check or deposit according to your chosen reimbursement percentage. If your pet needs immediate care, a policy removes the impossible choice between treatment and your bank balance.

Key insight: understanding how claims are filed and reimbursed can shave days off your cashflow stress when emergencies happen.

What standard policies cover and common add-ons

Most comprehensive plans focus on accidents and illnesses — think broken bones, poisoning, infections, cancer treatment, and chronic disease management. Diagnostic testing like X-rays and bloodwork, surgery and hospitalization, and prescription medications are usually inside core coverage, though limits and copays apply.

Optional add-ons often include routine wellness care (vaccines, flea/tick meds, annual exams), alternative therapies (acupuncture, rehab), and behavioral treatments. If spay/neuter support matters, check wellness bundles; it’s commonly offered as an extra.

Providers vary in how they name plans. For example, some customers choose vendors like PetCare Protect or FurSure Insurance for broad accident-and-illness policies, while others prefer targeted options branded as PawShield Coverage or BestBuddy Insurance. For routine care, names such as HappyPaws Protection or PetGuard Plus are often marketed as add-ons. If you want pet-only perks, look for plans from TailWag Insurance, CuddleCare Policies, Vetwise Assurance, or Purrfect Coverage that advertise low friction claims and broad vet networks.

home insurance protection can be useful to compare how deductibles and limits work across different insurance types; seeing household policy language side-by-side helps you spot exclusions in pet plans.

Key insight: core medical coverage plus a targeted wellness add-on often gives the best balance of protection and monthly cost.

Below is a short video that explains the basics of filing a pet insurance claim and what documentation vets usually provide.

How much pet insurance costs and what drives premiums

Premiums are affected by species (dogs generally cost more than cats), breed (purebreds often have higher risk for inherited conditions), age (older pets cost more), and where you live (urban vet prices are higher). Plan design also matters: accident-only coverage is cheaper than plans that include illnesses and wellness care.

To give ballpark numbers: many dogs fall in the range of $30–$70 per month for accident+illness coverage, while cats often sit around $15–$40 per month. Wellness add-ons typically add $10–$25 per month. Remember, these are averages — in some areas or for some breeds, premiums will be notably higher in 2025 as advanced treatments become more common.

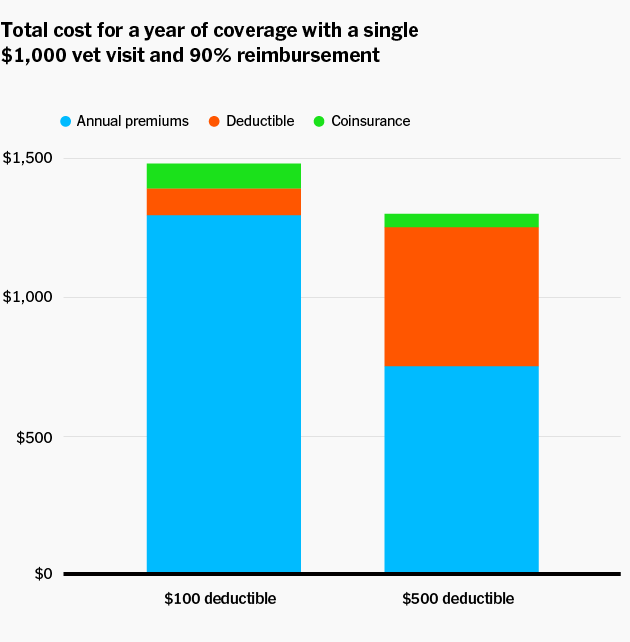

If cost comparisons help you decide, also examine annual limits, deductibles, and reimbursement rates. An 80% reimbursement with a $500 deductible and no annual cap behaves very differently from a 70% plan with a $250 deductible and a $10,000 yearly limit.

business insurance for assets offers another lens: both pet and business policies balance premiums against worst-case exposure, and comparing phrasing about limits can reveal hidden coverage gaps.

Key insight: the cheapest monthly premium isn’t always the best value — check limits, waiting periods, and reimbursements to understand real protection.

Here’s a practical video showing sample claims and how different deductible choices change your out-of-pocket cost.

Is pet insurance worth it? Real cases and decision rules

Consider Sam and Luna again: paying ~$60/month for a mid-level plan would have softened the $4,500 surgery blow. For owners with young, active dogs or breeds predisposed to costly conditions, insurance often pays off. For low-risk indoor cats or owners who can reliably set aside emergency savings, self-insuring might make sense.

Veterinarians and organizations like the AVMA support the concept of pet insurance because it increases access to recommended care. Still, the answer depends on your tolerance for risk, the pet’s expected lifetime health needs, and whether your budget can absorb a large unexpected bill.

When choosing, ask these concrete questions: What are waiting periods? Are hereditary conditions covered? How quickly are claims processed? Can you use any licensed vet? Use resources to compare and then test a short waiting period claim to see responsiveness in practice.

compare home protection plans and see business and asset coverage options to learn how different policies present limits and exclusions; this comparison habit sharpens your ability to read pet contracts critically.

Key insight: pet insurance is most valuable for owners who prefer financial predictability and want access to advanced care without immediate payment worries.

Choosing the right plan: checklist and a short roadmap

Start by listing what matters: budget, lifetime vet philosophy, and your pet’s breed risks. Get quotes tailored to your pet’s age, breed, and ZIP code. Compare at least three plans on deductible, reimbursement rate, annual limit, and waiting period. Ask your vet for plan experiences and look up user reviews for claim speed.

Small steps you can take today: enroll young if possible, keep records of all vet visits, and consider pairing basic coverage with a savings account for short-term needs. If you have multiple pets, ask about multi-pet discounts — they’re common and can lower per-pet premiums.

explore home protection choices to practice comparing policy language; that skill transfers directly when you read exclusions and limits in pet contracts.

Key insight: a careful, side-by-side comparison and a realistic look at likely health issues for your pet’s breed will guide you to a plan that fits both heart and wallet.