As America’s population ages, planning for long-term care is no longer optional — it’s a financial and emotional imperative. Take Maria, a retired teacher in her late 60s who lives alone and loves gardening. After a neighbor’s fall, Maria started asking questions: what happens if she needs help with bathing or managing meds, who makes decisions if she can’t, and how will she pay for care without depleting the savings she hopes to leave to her children? Current trends make that urgency clear: someone turning 65 today faces a nearly 70% chance of needing long-term care at some point, and median monthly costs in 2025 run at about $6,077 for assisted living and $9,555 for a semi‑private nursing home room. This article walks through practical planning steps — from spotting early signs of decline and sizing up ADLs/IADLs, to comparing traditional and hybrid insurance, to legal documents and community supports like Area Agencies on Aging. Along the way you’ll meet Maria again, see realistic scenarios, and get concrete resources so you can build a care plan that protects dignity, relationships and assets.

En bref — key takeaways : Start early to avoid rushed decisions; assess ADLs/IADLs to match services; mix funding (savings, HSAs, insurance) to reduce risk; create legal documents (POA, advance directives) to keep control; use local resources and geriatric care managers to coordinate care. These moves help preserve independence and reduce stress for families.

Long-term care insurance types and what they cover

When Maria began comparing options she found two clear paths: traditional long-term care (LTC) policies and hybrid products that blend life insurance with LTC benefits. Traditional LTC pays for services like in‑home aides, assisted living and nursing homes when you meet a benefit trigger; hybrids — offered by companies with names like LifeSpan Assure and FutureNest Insurance in hypothetical market examples — let you tap a death benefit for care or leave a payout to heirs if unused.

Understanding how policies pay benefits matters: look at elimination periods, daily or monthly benefit limits, and inflation protection. For a plain primer on policy mechanics, see how different policies work. Insight: choosing the right product depends on health, family history and what you want to leave behind.

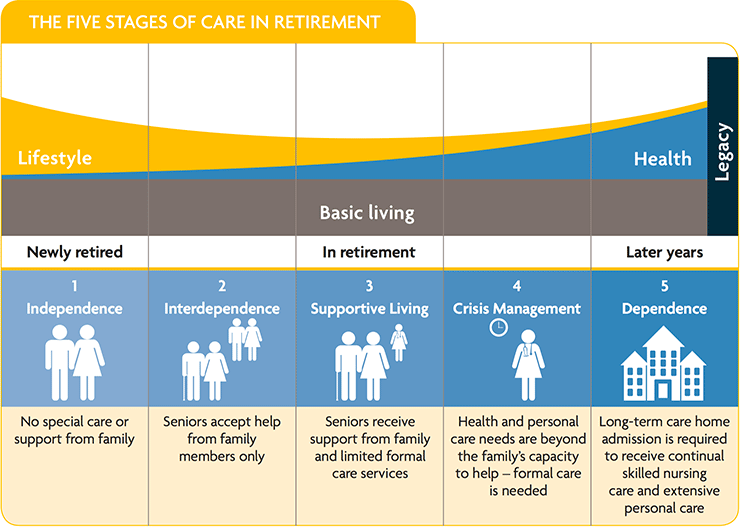

Assess needs early: ADLs, IADLs and timing

Start by tracking Activities of Daily Living (ADLs) like bathing, dressing, eating, toileting and mobility; needing help with two or more ADLs is often the threshold for benefits. Also watch Instrumental Activities of Daily Living (IADLs) — tasks such as managing finances, preparing meals, taking medications and driving — because declines there often arrive sooner and warn you to plan.

Maria’s case study: after she forgot bills twice and burned a meal, her family arranged a home safety check and a geriatric assessment. That early intervention delayed the need for residential care and clarified services she might need later. Insight: spotting IADL trouble early creates the most options and reduces crisis-driven choices.

Financial strategies: self-funding, HSAs, traditional and hybrid policies

Money is often the sticking point. Options include self-funding with dedicated savings, using Health Savings Accounts (HSAs), buying traditional LTC insurance, or opting for hybrid solutions that combine life insurance and LTC benefits from providers similar to hypothetical names like CareShield or GoldenYears Insurance. Each choice has trade-offs: traditional policies can be cheaper early but are “use it or lose it”; hybrids cost more but leave a benefit to heirs if unused.

Remember that Medicare won’t cover long-term custodial care, while Medicaid can but requires strict income and asset rules plus a look‑back period. Tax rules can help: premiums and HSA distributions can be tax-advantaged depending on your situation. For related planning on unconventional incomes and protections, check resources for coverage options for nontraditional careers and consider how disability safety nets fit with long-term plans via disability insurance as a backup. Insight: a blended funding approach usually offers the best balance between cost and protection.

Legal documents and care coordination that protect wishes

Legal prep makes daily life smoother when health changes. Key documents include a durable power of attorney for finances, a healthcare proxy, and a living will/advance directive. Maria signed these with an elder-law attorney and saved her family months of stress during a later hospitalization.

Beyond papers, use a geriatric care manager to coordinate services, especially if family is distant. These pros assess needs, arrange home care, and oversee transitions to assisted living or memory care. Insight: clear legal documents plus professional coordination preserve autonomy and reduce family conflict.

Home adaptations, community supports and aging in place

Most people prefer to stay at home. Aging in place is achievable with sensible changes: add grab bars, improve lighting, remove trip hazards, and consider ramps or stairlifts. Programs and grants can defray costs — learn more about preparing your home with tips at preparing your home for aging in place. These upgrades not only protect mobility but also delay expensive residential moves.

Community resources matter: Area Agencies on Aging, adult day centers and respite services give social contact and caregiver relief. Organizations and local programs can also connect you with home health agencies and waiver programs like the MI Choice Waiver that keep people safely home. Insight: modest home investments plus community services dramatically extend independence.

Putting the plan into action and revisiting it regularly

Create a living plan: list contacts, document finances, assign responsibilities and schedule annual reviews. Include contingency triggers — for example, two falls in six months or inability to manage medications — that prompt reassessment. Maria and her family set annual check-ins tied to medical visits, which kept everyone aligned.

Also, review insurance and funding choices every 3–5 years as markets and policies evolve. For health coverage overlap and practical tips, see health insurance basics and consider cyber and other modern risks that affect seniors’ assets at digital protection resources. Insight: a plan that’s written down and updated turns worry into a manageable routine.

Choosing providers and comparing offers — practical checklist

When comparing companies — whether real insurers or hypothetical brands like SeniorShield, SecureAging, HeritageCare, EverCare Protection or AgeWise Coverage — focus on exclusions, inflation riders, elimination periods, and financial strength ratings. Ask for sample policy scenarios that show real-life payouts over 5–10 years.

Also validate provider reputations, read sample contracts, and run quotes with different start ages to see premium trajectories. If you freelance or have irregular income, factor that into your affordability assessment and review options at alternative insurance guides. Insight: apples-to-apples comparisons reveal the true cost and value of each policy.

Where to get help locally and online

Start with your state’s Area Agency on Aging and local elder services for practical supports, and hire an elder‑law attorney for legal documents. Geriatric care managers and financial planners who specialize in retirement can create coherent, realistic plans. Search trusted directories and read client reviews before hiring.

Online resources and comparison tools help demystify coverage, but pair online research with professional advice for complex cases. For example, someone balancing small business risks should also review protections like business and personal policy interactions. Insight: combining local programs, professionals and smart online tools produces the most resilient plan.