Insurance prices feel mysterious until you strip away the jargon: premiums are basically a price tag for the risk an insurer accepts. Take Sam, a 34‑year‑old who juggles a downtown commute, a mortgage on a renovated house and a rescue dog — his annual bill is shaped by everything from his driving record to whether his roof was updated after last year’s storm. In 2025 insurers blend traditional actuarial analysis with real‑time tech: telematics and smart home sensors feed models like RiskAssess and RiskMatrix, while market shifts and regulations nudge tools such as PremiumPlanner and PolicyPricer under the hood. The result is a premium that reflects individual behavior, property traits, policy choices and broad economic forces. Understanding the levers — personal habits, property value, claims history, policy structure and market conditions — gives you leverage to lower costs and choose smarter protection. This article follows Sam’s decisions to show how insurers price risk, which tradeoffs matter most, and where simple fixes can make a real dent in your bill.

En bref — key takeaways: Personal behavior (age, driving, health) and claims history drive big swings in premiums; property location and security upgrades reduce home rates; choosing higher deductibles lowers short‑term cost but raises out‑of‑pocket risk; telematics and safety tech create new discount paths; macro forces and regulations still shape overall market pricing.

Personal and behavioral factors that influence insurance premiums

Insurers start pricing with a person-level risk profile: things like age, occupation, driving history and health status signal expected claims. Sam’s speeding ticket and two minor claims from five years ago make his auto quotes higher than a peer with a clean record.

Health choices also matter: smoking, chronic conditions and medication histories feed health models used in underwriting. For practical guidance on lowering health costs and picking plans, see this health insurance tips resource. Final insight: improving everyday habits and keeping records tidy often yields the fastest savings.

How driving records and telematics reshape auto premiums

Traditional factors like accident history and mileage still matter, but telematics changes the game by replacing estimates with live behavior data. Devices or apps monitor speed, braking and time of day — insurers reward consistent safe driving recorded by telematics programs in their PremiumPulse dashboards.

Sam installed a telematics app and saw an offer drop from several carriers after 6 months of steady scores. For a primer on the types of auto protection to consider, consult this guide to auto insurance coverage benefits. Insight: telematics converts good driving into tangible discounts, but watch privacy terms carefully.

Property, location and security: why where you live changes the bill

Insurers price homes based on location risk (flood, fire, crime), replacement cost and the property’s physical state. Sam’s renovated bungalow in a neighborhood with a nearby fire station attracted a lower quote than an equivalent dwelling in a flood‑prone zone.

Simple safety upgrades — alarms, sprinklers, reinforced entry points — reduce expected loss and often trigger discounts. If you rent rather than own, review fundamentals in a renters insurance coverage article. Final insight: targeted upgrades and knowing local hazard profiles deliver disproportionate savings.

Upgrades, deductibles and how much coverage to choose

The coverage limit and the size of your deductible are among the quickest levers to tune premiums. A higher deductible lowers the premium but raises your immediate cost after a claim. Learn to compare tradeoffs with an explainer on understanding deductibles.

Sam balanced his premium and emergency savings by choosing a mid‑range deductible and adding endorsements for sewer backup after a local storm. Insight: pair deductible choices with an emergency fund, and your premium decisions become strategic rather than reactive.

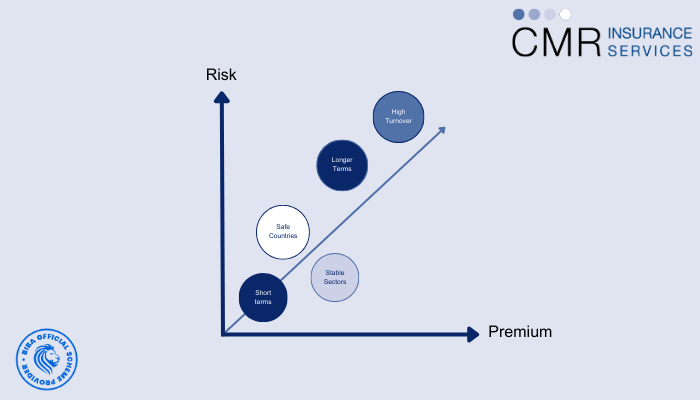

Policy design, claims history and legal context that shape pricing

Underwriting blends individual data and legal constraints. Insurers use actuarial models to forecast frequency and severity of claims, then apply regulatory rules that vary by jurisdiction. In some areas legal changes around liability or compensation can shift whole markets, so carriers update rates accordingly.

Claims history is a strong predictor: frequent small claims often raise flags more than a single, well‑documented major loss. For newcomers comparing options, this insurance beginners guide clarifies how claims affect future pricing. Insight: avoid frivolous claims and document everything when losses occur — your future premiums depend on it.

How insurers use data, analytics and market signals

Modern pricing mixes historical losses with real‑time signals. Tools named in industry discussions — like CostDriver Analytics, RateReveal and CostFactor Insights — help translate raw data into price adjustments. Regulators require fair practices, so models incorporate checks to limit discriminatory outcomes.

Insurers also monitor fraud trends and adjust underwriting to control losses; learning about scams helps consumers too, as seen in this piece on insurance fraud and scams. Finally, specialized policies — life, disability or business coverage — have their own drivers: read basics at life insurance basics or disability insurance income. Insight: data and regulation shape fair pricing, but proactive consumer choices still move the needle.

Technology, safety features and the future of premium pricing

Adoption of safety tech — from advanced driver assistance to smart sensors — aligns incentives: fewer incidents mean lower payouts and lower premiums. Carriers increasingly offer usage‑based products and rewards through platforms that advertise InsuranceInfluence and InsureImpact metrics.

For pet owners like Sam, add another layer: pet health and breed history often steer the cost of coverage. A quick overview at pet insurance explained shows how preventive care and records reduce long‑term expenses. Insight: invest in proven safety tech to lock in discounts and protect assets.

Putting it together: a practical checklist for lowering premiums

Start by cleaning up your records, bundling policies when possible, and comparing quotes with an eye on coverage, not just price. Use telematics to prove safe driving, invest in verified home safety upgrades, and match deductibles to your financial buffer. For one‑stop policy comparisons see insurance policies explained.

Sam’s story shows that targeted action — a telematics install, a roof upgrade and a careful deductible choice — cut his overall insurance spend while improving protection. Final insight: premiums are transparent once you map the variables; act on the ones you control and track the rest with tools like PolicyPricer and RateReveal to stay ahead.