En bref — SecureLife thinking: get coverage early, choose a term that matches your mortgage or parenting years, aim for 10–12x your income, and compare providers before you buy. Consider policies that convert if your needs grow, and remember employer coverage rarely replaces what a family needs. Use reliable guides to check what fits your stage and budget.

Maya’s 8:45 pm moment—she’s doing the dishes, kids asleep, and that small what-if creeps in: who pays the mortgage if she’s gone? This article walks through the essentials of life insurance so parents like Maya can act, not panic. You’ll get clear comparisons between term and whole life, a practical rule of thumb for coverage, and easy next steps to actually buy a policy that protects your family.

We’ll follow Maya as she evaluates quotes, talks to her partner, and locks a plan in place. Along the way you’ll see how brands like FamilyShield, FutureGuard, and niche offerings such as SafeHaven Insurance or PeacePath Insurance are pitched—and what really matters when you compare numbers. By the end you’ll know what questions to ask and how to avoid common traps.

Life insurance basics for parents: why coverage matters now

Life insurance is not morbid—it’s practical. If someone depends on your paycheck, caregiving, or both, life insurance steps in with a tax-free lump sum that can replace income, pay off the mortgage, and cover childcare or tuition.

Research keeps showing the gap: many households would face hardship within months of losing their primary earner. That’s why starting with a simple quote and plan is the best way to turn worry into action. Insight: a small monthly premium today can prevent years of financial strain later.

What is life insurance and what can the payout do for your family?

At its core, life insurance is a contract: you pay a premium, the company pays a death benefit while the policy is active. Families typically use that money to replace lost income, clear debts like a mortgage, pay for kids’ education, and cover funeral costs.

For example, a payout can allow a surviving partner to stay in the family home or fund three to five years of living expenses while they retool their finances. Insight: think of the death benefit as a bridge—financial breathing room to make thoughtful decisions instead of rushed ones.

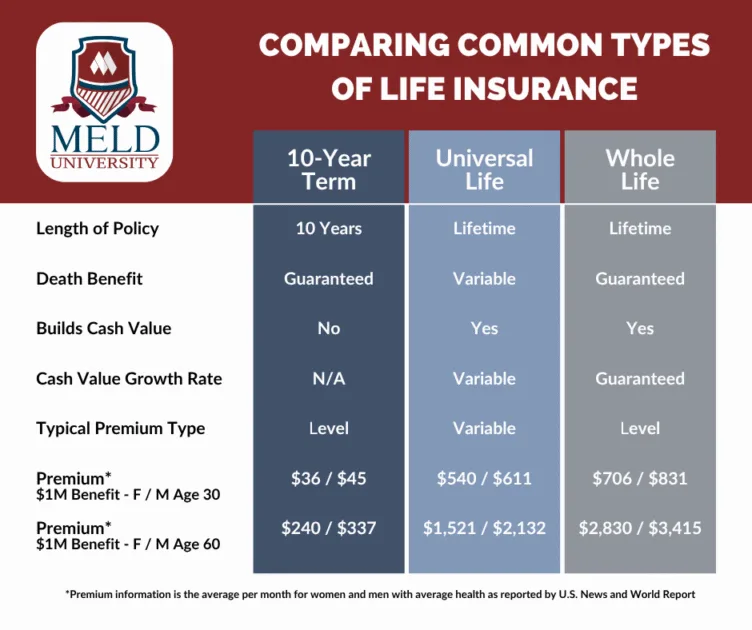

Term life vs whole life: which one fits your family’s needs?

Term life is simple and affordable: coverage for a set period (10, 20, or 30 years) with low premiums. It’s ideal for parents who need high protection while raising kids or paying a mortgage.

Whole life lasts for life and builds cash value you can borrow against, but premiums are significantly higher—sometimes up to ten times the cost of term. For most families, term offers the best cost-to-protection ratio. Insight: if your goal is to protect your family’s lifestyle affordably, start with term.

How much coverage should you buy?

A practical rule of thumb is 10–12x your annual income, plus mortgage and education costs. So if you make $80,000, consider roughly $800,000–$960,000 as a starting point before adjusting for debts and future goals.

Another quick method: Annual income × 10 + mortgage balance + other debts + estimated college costs = recommended coverage. Use tools and calculators to refine this for your situation. Insight: aim for a coverage number that keeps your family’s options open, not one that creates false comfort.

When to buy and common myths that stop people

The right time is sooner rather than later: premiums rise with age and health changes can limit options. Buying in your 20s or 30s locks in lower rates and gives your family longer protection.

Common myths—“I’m young, I don’t need it,” or “I get enough from work”—are risky. Employer policies often cover only 1–2x salary and vanish if you change jobs. Insight: securing a personal policy is the decision that stays with you, not your employer’s benefits.

Simple three-step path to getting covered

Step 1: Get quotes online and compare companies with strong financial ratings. Trusted marketplaces and guides help speed this up—check an insurance beginner’s guide to start. Step 2: Choose a term length and amount that matches your life stage—20 or 30 years are common for parents.

Step 3: Complete the application. Some plans need a medical exam; others offer simplified underwriting. If you prefer guidance, read expert tips on the right insurance tips page before you call. Insight: getting a quote takes minutes; the payoff lasts years.

Real-life example: Maya’s decision and numbers

Maya is 35 with two kids, a $300,000 mortgage, and household income of $95,000. She chose a 30-year term with $750,000 coverage—enough to cover income replacement, mortgage payoff, and education funding.

Her monthly cost was close to market estimates for healthy 35-year-olds—an accessible amount that replaced a major financial risk. She compared offers, read an insurance policies explained resource, and selected a company with solid ratings. Insight: real families often find a sustainable premium once they quantify the gap.

Where to learn more and where to compare quotes

Reliable resources can help you avoid pitfalls. For home-and-family protection context, see a practical piece on home insurance protection, and loop back to the insurance beginner’s guide for step-by-step checklists.

Brands and product names—like LegacySecure, TrustGuard Life, EverProtect, and GuardianPromise—may appear in quotes, but compare the numbers and policy terms rather than the buzzwords. Insight: the company name matters less than the death benefit, exclusions, and claim reputation.

Final practical tips before you buy

Lock a rate while you’re healthy, consider a term that matches your mortgage or kids’ ages, and name clear beneficiaries. If your situation is complex—estate planning, business ownership, or a lifelong dependent—talk to an advisor about permanent solutions.

Keep one sentence as your decision rule: buy what your family would need to maintain their lifestyle for several years, not just to pay immediate bills. Insight: protection is the baseline—investing for growth comes next, and both can live in the same plan if you plan deliberately.