In 2025, young families face a mix of familiar risks—illness, accidents, vehicle damage—and newer pressures like rising healthcare costs and climate-driven weather events. This guide walks through the core protections every young household should consider, from health and life to renters/home and disability, and explains how to prioritize coverage when budgets are tight. Using the story of Anna and Marcus, new parents balancing a mortgage and childcare, we show practical choices: which policies to buy first, how to layer add‑ons like an umbrella policy, and when to favor term life over whole life. You’ll also get clear action steps to compare quotes, spot discounts, and avoid common pitfalls that eat premiums or void claims. Expect concrete examples, a few quick calculators you can run in your head, and links to reputable explainers so you can dig deeper on topics like riders, disaster protection, and income‑replacement solutions.

En bref: Start with health to avoid catastrophic bills; secure income via term life and disability; protect home or rental and belongings; add umbrella for liability; shop smart — compare, bundle, and check credit/discounts. These moves form a basic YoungFamilyShield that keeps day‑to‑day life intact while you build savings and plan for the future.

Essential coverages for young families: what to buy first

When Anna and Marcus welcomed baby Leo, their priority list shifted. They realized that a single hospitalization or loss of income could derail plans. For most young families the purchase order is simple: health insurance, term life to replace income, and disability insurance to protect against inability to work.

Health plans limit out‑of‑pocket exposure and preserve savings; term life provides a focused safety net during high‑need years; disability replaces paychecks if illness or injury prevents work. Start with policies that cover basic survival costs—mortgage/rent, childcare, and outstanding debts—to create a reliable FamilyFirst Coverage baseline.

Health insurance: avoid the financial shock

Health coverage is the most immediate protection for young families. Medical bills are still a leading cause of household financial distress, so a comprehensive plan for routine care and emergencies is a must. Look for plans with a strong provider network and reasonable out‑of‑pocket maximums.

Tip: compare total annual cost (premiums + expected out‑of‑pocket) rather than premiums alone. If you need a primer on terms like deductible, copay, and coinsurance, check this insurance glossary to decode policy language. Strong insight: prioritize predictable access to pediatric care and hospital coverage—these reduce stress and keep savings intact.

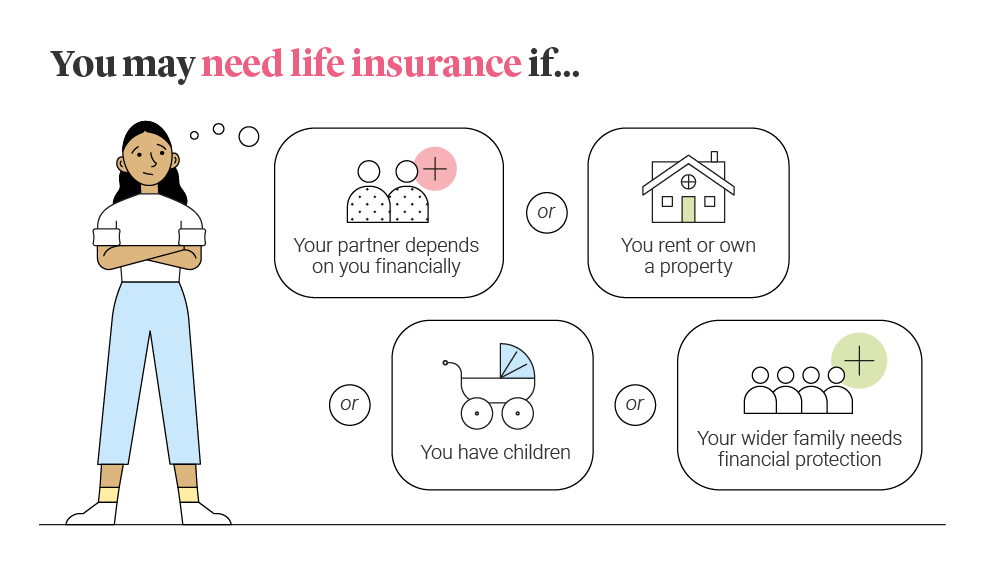

Life insurance: affordable protection for dependents

For many young families, term life insurance provides the best cost/value ratio. It covers a fixed period—often 10, 20, or 30 years—matching the years when dependents rely most on your income. Anna chose a 20‑year term that covers the mortgage and childcare until the kids are more independent.

Consider riders and add‑ons that matter: child riders, critical illness riders, and waiver of premium for disability. If you want to understand common rider options, read about life insurance riders. Final note: aim for coverage equal to roughly 5–10x your household income, adjusted for debts and future education costs.

Income protection and disability: the often‑overlooked safeguard

Disability insurance is the unsung hero for young earners. A serious injury or chronic illness can remove your primary earner from the payroll for months or years.

Short‑ and long‑term disability policies replace a percentage of wages and should be evaluated for waiting periods and benefit length. To compare how benefits replace income and how policies define disability, see this guide to disability insurance income. Insight: prioritize long‑term coverage that bridges to social security or employer benefits—this is where families avoid long-term financial collapse.

Home, renters and natural disaster protection

Whether you own a house or rent, protection for where you live is essential. Homeowners insurance covers the structure and personal property; renters insurance protects personal items and liability. For renters, a low‑cost policy can replace devices, furniture, and provide temporary housing assistance after a loss.

With increasing climate volatility, consider disaster add‑ons or separate policies for flooding and large storms. Learn what disasters require extra coverage at natural disaster insurance. Insight: a small extra premium for targeted disaster protection can prevent ruin after a single catastrophic event.

Auto and young drivers: keep premiums manageable

For families with a new driver, auto insurance premiums can surge. Policies should balance liability limits with collision/comprehensive coverage based on vehicle value and driving habits. Bundling auto and home/renters policies can unlock discounts and simplify claims.

Young drivers can reduce costs through defensive driving courses, good grades, and telematics programs. Practical advice is in this young drivers insurance resource. Final point: invest in higher liability limits if you have significant assets or a growing net worth—it’s inexpensive protection compared to potential lawsuits.

Smart add‑ons: umbrella, pet, and flexible endorsements

An umbrella policy extends liability protection when autos or homeowners limits aren’t enough. Pet insurance can offset unexpected veterinary bills and preserve savings. Also consider flexible endorsements to cover growing needs; learn about endorsements and customization at insurance endorsements.

These extras form part of a layered approach—think of them as upgrades to the core SafeNest Coverage that keep unexpected hits from spiraling into long-term setbacks.

How to choose—and keep—policies that fit

Start by listing your fixed expenses, debt obligations, and short‑term savings goals. This clarifies how much income replacement you need and which property protections are essential. Anna and Marcus wrote a simple spreadsheet showing mortgage, childcare, and monthly bills to set coverage targets.

Get at least three quotes, ask about bundling discounts, and verify claim service quality before buying. Use tools like smart quote comparators and read about premium drivers at insurance premium factors. A practical renewal habit: review policies annually—see insurance renewal tips—and adjust coverage as income or family size changes. Insight: yearly checkups keep costs fair and coverage aligned with life.

Common mistakes to avoid

Two frequent errors: underinsuring (too little coverage) and buying duplicate policies. Both waste money or leave gaps when you need help most. For a deep dive into myths and traps, consult insurance myths debunked.

Final takeaway: buy the essentials first, then layer wisely. The goal is a practical StarterShield Insurance that grows with your family.