When Maya bought her first home in 2025 she felt like she needed a translator for insurance-speak. Policies were full of terms that sounded technical but actually map directly to real choices: Actual Cash Value (ACV) vs Replacement Cost (RC), separate hurricane deductibles, or whether a classic car qualifies for an agreed value policy. This glossary cuts through the noise with a friendly voice, real-world examples and a running story about Maya as she calls an adjuster after a storm, debates OEM parts for her repaired car, and weighs an endorsement for her grandma’s jewelry. Expect clear definitions, practical tips for claims, and quick pointers to tools like SureGloss and PolicyPals that help you look up terms fast. We’ll also flag where words have legal weight — for instance, insurable interest and subrogation — so you know when a claim or contract clause can change outcomes. Read on to build confidence with the language that shapes premiums, coverages and settlements; by the end you’ll feel more fluent and less likely to be surprised at renewals or during a claim.

En bref — key takeaways at a glance:

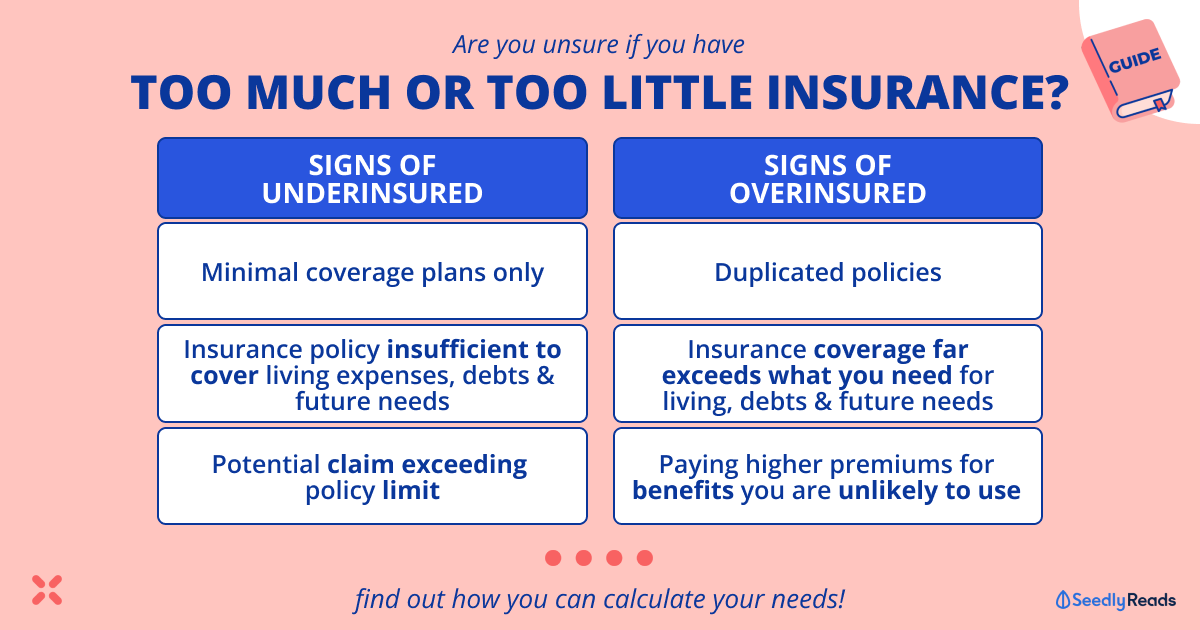

Actual Cash Value vs Replacement Cost: ACV = replacement minus depreciation; RC pays to replace with new items.

Deductible: Your out-of-pocket before insurer pays; different per peril (e.g., wind/hail).

Liability vs Physical Damage: Liability covers others’ injuries/property; physical covers your property or vehicle.

Endorsements & Exclusions: Small policy changes that can add or remove coverage — read them carefully.

Claims basics: File promptly, mitigate damage, keep receipts; adjusters, appraisals and reserves drive settlement timing.

Comprehensive insurance glossary: key terms simplified for homeowners and drivers

Start with two pillars: policy is your written contract and premium is what you pay for it. Policies contain declarations (the “who, what, where” page), conditions (what both you and the insurer must do), and exclusions (what’s not covered). Maya learned this when her declarations page listed a separate wind/hurricane deductible — a special amount that applies only to named storm claims, which changed her potential out-of-pocket substantially.

Think of an insurance policy like a recipe: ingredients (coverages), cooking rules (conditions), and a small print list of “don’ts” (exclusions). If you aren’t sure how a term affects you, tools like InsureLex or CoverWords can translate legal phrasing into everyday decisions. Final insight: understanding the structure of a policy prevents nasty surprises when you need to use it.

Core auto and property terms: ACV, RC, deductible, liability made clear

Actual Cash Value (ACV) means the value of property at the time of loss — essentially replacement cost minus depreciation. For example, if a five-year-old laptop is stolen, an ACV settlement reflects its used value, not what you paid new.

Replacement Cost (RC) pays to replace with like kind and quality without deducting for age. Homeowners who choose replacement cost for their dwelling or contents trade higher premiums for fuller recovery after a loss. Maya opted for RC on her roof after getting quotes that showed how fast roofing prices rose in her area.

Deductible is your agreed contribution before insurer pays; some policies have specialized deductibles for hurricane or earthquake events. Picking a higher deductible lowers your premium but raises immediate cash needs when a covered event happens — a tradeoff worth testing with a quick budget run-through.

Liability coverage pays for injuries or property damage you cause to others. It’s different from physical damage coverages like collision (hits) and comprehensive (theft, vandalism, weather, animal strikes). Remember: liability protects your assets if someone sues.

Insight: match deductible choices to your emergency savings and prefer RC when replacement costs in your area rise quickly.

Homeowners and renters vocabulary: what to watch for in your policy

Personal property covers movable items like furniture and clothing. Options such as Scheduled Personal Property or Valuables Plus let you insure high-value items—jewelry, art or collectible coins—at agreed limits and appraised values so you’re not limited by standard sub-limits.

Additional living expense (Loss of use) pays the extra cost of living elsewhere if your home is uninhabitable after a covered loss. Maya rented a short-term apartment and used receipts to document meals and lodging; the insurer reimbursed reasonable expenses under that coverage.

Ordinance or law coverage steps in when updated building codes force more expensive rebuilds than the original structure — useful after a major fire when new materials or safety features are mandated. If you care about full rebuilding rather than minimal repairs, consider endorsements and discuss dwelling replacement cost plus/guarantee with your agent.

Tip: always inventory your valuables with photos and receipts; tools like GlossaryGuard or InsureVocab make it easier to prepare schedules and appraisals.

Insight: extra coverages for high-value items and ordinance compliance can save you thousands; schedule anything irreplaceable.

Auto-specific terms and specialty coverage: classic cars, electronics, and rental help

Additional coverage for sound, picture and data devices covers audio/visual gear not permanently installed in a vehicle — think high-end stereo systems and dash cams. If you’ve customized your ride, list those items so they’re included.

Customization refers to after-market accessories like chrome rims or body kits; an OEM endorsement can protect you from aftermarket parts being used after a crash. For collectors, classic car insurance and partners like Hagerty or an agreed value policy can guarantee the sum paid on a total loss rather than an ACV number.

Rental reimbursement (also called Loss of Use) helps with alternate transport while your car is repaired. And if you drive someone else’s car often but don’t own one, named non-owner (NNO) coverage might be what you need. For high-risk drivers, SR-22/FR-44 filings may be required — they’re proof to the state that you carry the required liability limits.

Tools like PolicyPals and ClaimClear speed comparisons and help with claims documentation when you need to prove custom parts or agreed values.

Insight: specialty endorsements for classic cars and custom gear protect value; document everything before a claim.

Claims, policy mechanics and key financial terms every policyholder should know

Claim is your request for payment after a covered loss; the claimant can be you or a third party. After filing, an adjuster investigates, an appraisal may determine damage value, and the insurer may apply depreciation unless you have replacement-cost coverage. Maya learned that keeping dated photos and repair receipts makes settlements faster and more accurate.

Indemnification is the principle that insurance aims to restore you to your pre-loss financial position, not to profit you. This is why subrogation allows the insurer to pursue a liable third party after paying your claim. If a neighbor’s tree fell on your garage, your insurer might pay you and then seek recovery from the neighbor’s policy if negligence is proven.

On the company side, terms like premium, loss reserves, loss ratio and risk-based capital explain how insurers price cover and stay solvent. When rates rise, it often traces back to higher claims frequency or catastrophe losses, not just corporate greed.

If you want a clean reference that translates legal phrasing into plain English, RiskSimplify, TermTrust, and WarrantyWise are handy; combined with ClaimClear they make claims and policy review less cryptic. Final insight: proactive documentation and knowing the chain (file claim → adjuster → appraisal → settlement) shortens timelines and reduces disputes.