Life insurance vs. annuities is a question that pops up when people start thinking seriously about money, family and retirement. Imagine Alex, a 48-year-old small-business owner who met an advisor at Lifetime Financial after a health scare; Alex wanted to know whether to buy additional coverage for his two kids or convert some savings into an income stream he couldn’t outlive. This article breaks down the essentials—how each product works, who benefits most, and how to combine them in a plan that fits changing priorities. You’ll see concrete examples, real-world trade-offs, and practical steps to compare offers from companies like LifeGuard Assurance, AnnuityPlus and TrustLife Insurance. By the end, you’ll be able to explain the core difference in plain English: life insurance replaces income for others after you die, while annuities convert savings into income for you while you live. Expect guidance on underwriting, taxes, liquidity and product types—plus a short case study following Alex’s decisions with input from an advisor at Lifetime Financial—so you can take the next step with confidence.

En bref: Life insurance = death benefit to protect loved ones; Annuities = guaranteed income for the policyholder; choose based on whether you need to replace future earnings or secure retirement cash flow; consider combining both for a balanced plan; check underwriting, tax treatment and surrender terms before buying.

Understanding the core difference: Life insurance vs annuities explained

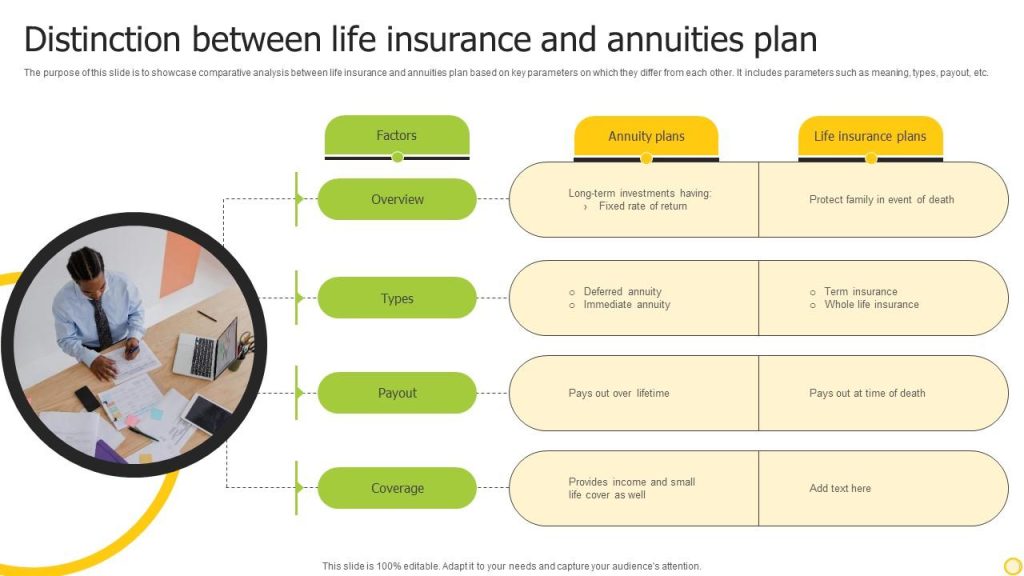

At their heart, life insurance and annuities tackle opposite financial risks. Life insurance covers mortality risk—the danger of dying too soon and leaving dependents without income. Annuities address longevity risk—the risk of outliving your savings.

Life insurance typically pays a death benefit to named beneficiaries, while annuities pay a regular income to the contract owner. Both are issued by insurers, but their purposes, timing of payments and underwriting differ sharply. This contrast was central to Alex’s meeting with a planner: he needed to decide whether to prioritize a larger death benefit for his children or to transform a chunk of capital into steady retirement income.

How life insurance works in practice

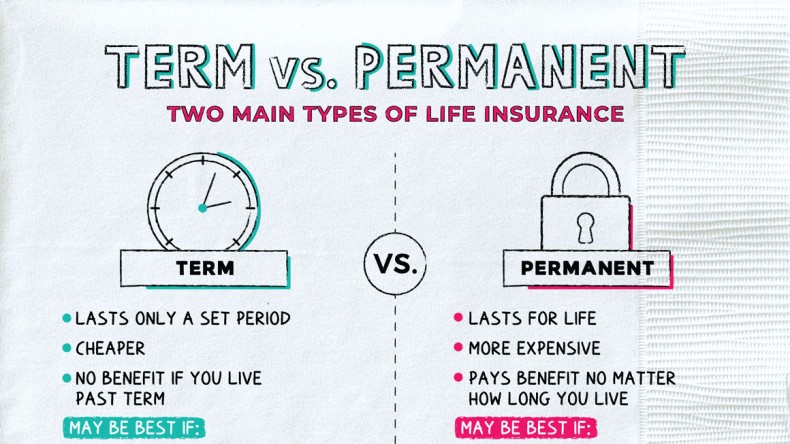

Life insurance comes in two main flavors: term (coverage for a set period) and permanent (whole or universal life, which can build cash value). Underwriting usually involves health checks, so younger and healthier applicants get lower premiums.

Use cases are clear: replace income for dependents, cover a mortgage, or fund a child’s education. For people like Alex with dependents, a term policy can be a cost-effective shield during working years, while a permanent policy may serve estate or legacy goals. For a primer on policy features, see this how policies work.

Key insight: choose life insurance when the priority is to ensure family financial stability after your death.

How annuities turn savings into lifetime income

An annuity is a contract where you pay either a lump sum or periodic amounts to an insurer and later receive regular payments. They come in forms like fixed, indexed or variable, and can be immediate or deferred.

For retirees worried about market swings, annuities offer predictability. Companies such as AnnuityPlus, EverSafe Annuities and Infinity Annuities market products that guarantee income for life or for a set term. If you want to understand tax timing and withdrawals, read more on annuity tax treatment.

Key insight: annuities are best when the primary goal is a reliable retirement paycheck rather than leaving a large death benefit.

When to choose life insurance and when an annuity makes sense

Deciding depends on life stage and priorities. If you’re building wealth and have dependents, life insurance usually takes priority. If you’re near or in retirement and your main worry is running out of money, annuities look more attractive.

Consider Alex again: at 48 he initially needed more protection, so his advisor at Lifetime Financial recommended increasing his term coverage, while setting aside a portion of savings to buy a deferred annuity at 60. That split matched his dual goals: protect dependents now, secure income later.

Signs life insurance is the right move

Life insurance is compelling when you have dependents, outstanding debts, or estate planning needs. It also makes sense if your employer coverage is limited or if you run a small business with partners who rely on you.

To explore basic policy types before choosing, check the life insurance basics guide. Remember: premiums and insurability matter—see how age and health affect cost at what affects premiums.

Key insight: prioritize life insurance when protecting others from financial hardship is urgent.

When an annuity may be the better option

An annuity is attractive if you’ve already accumulated retirement savings and want to convert that nest egg into predictable income. It suits those who prize stability over market upside.

Hybrid products and riders exist (for example, long-term care riders), so if long-term care is a concern, review options at long-term care resources. Also weigh liquidity constraints and surrender charges before committing.

Key insight: choose annuities if your main goal is predictable, guaranteed retirement income.

Combining products: a balanced plan with life insurance and annuities

It’s common to use both products. One funds the “what if” (your family if you die unexpectedly), the other secures the “what now” (income during retirement). Financial firms like SecureFuture Insurance and Guardian Life Plans often design solutions that layer protections.

Alex’s case study: he bought a 20-year term policy through TrustLife Insurance for protection and set up a deferred fixed-indexed annuity with AnnuityWise to begin payments at 65. His planner used scenario modeling so he could see trade-offs between leaving a legacy versus guaranteeing income. For a step-by-step on tailoring coverage, review customizing your coverage.

How a combined strategy can work

Practical combos include keeping term coverage while purchasing a small immediate annuity to handle essential monthly expenses. Alternatively, a permanent life policy with cash value can be tapped (carefully) to fund retirement needs or an annuity through a 1035 exchange.

Before converting any policy, understand tax consequences and surrender penalties—see guidance on policy changes at policy cancellation and changes.

Key insight: pairing life insurance and annuities can cover both family protection and lifetime income when structured to your priorities.

How to compare offers and pick the right provider

Comparing products requires looking beyond flashy guarantees. Focus on insurer financial strength, contract details, fees, liquidity and riders. Names like PeaceOfMind Coverage and LifeGuard Assurance may appear in quotes, but check ratings and policy language before deciding.

Start with clear questions: What are guaranteed vs non-guaranteed elements? Are payments fixed or indexed? What are surrender schedules and withdrawal penalties? For beginners, a practical primer is available at insurance beginner’s guide. When comparing quotes, also use tools like smart insurance quotes to get multiple offers.

Checklist for the contract review

Prioritize transparency. Confirm the tax treatment of proceeds, whether the death benefit changes if you take loans, and how beneficiaries are named. If you’re planning to borrow against cash value or convert to an annuity, consult a tax pro first.

Look at product illustrations and stress-test the income assumptions under different market scenarios. This helps you avoid surprises and ensures the contract supports your long-term plan.

Key insight: a careful contract review beats a low initial quote—protect certainty by reading the fine print and asking for scenario projections.

Final action steps for readers

Talk to a licensed advisor, gather quotes from multiple carriers, and map scenarios for your family and retirement goals. If you want a quick reference on coverage types and how deductibles or features interact with other protections, check policy comparisons and deductible guides.

Key insight: informed choices come from comparing products, understanding trade-offs, and aligning them to your personal timeline and dependents’ needs.