What affects your insurance credit score: explained — Insurance companies don’t just look at your driving record or the age of your home. They also build a specialized number from your credit file called a credit-based insurance score, and that number can move your premium up or down by hundreds or even thousands of dollars a year. Take the story of Alexis, a grad student who paid cash for her car and avoided credit cards: in states like Florida her thin or non-existent credit history translated into much higher auto premiums, even though she’s a careful driver. Behind the scenes insurers use proprietary algorithms that weigh things like payment history, credit utilization, and recent inquiries to estimate future claims. Because rules differ by state and companies tune models differently, the same person can get wildly different quotes depending on ZIP code and insurer. This piece walks through how those scores are built, why they matter in 2025, concrete ways to improve your standing with tools like CreditScoreBoost or advice labeled under CreditInsight, and practical alternatives—bundles, higher deductibles, safety features—that can blunt the financial sting while you work on your credit. Read on to understand what insurers really care about and how to push your PolicyScore in the right direction.

In brief: Credit-based insurance scores combine credit report signals and claims history; Payment history and credit utilization are the heaviest drivers; some states limit use of credit in pricing; improving scores (timely payments, lower utilization, fewer inquiries) often lowers premiums; and bundling or safety upgrades can deliver immediate savings.

What is an insurance score and how it’s calculated for premiums?

Insurers compute a specialized metric—often called an insurance score or PolicyScore—from your credit report plus claims data to predict the likelihood of future claims. The exact recipe is proprietary: companies weigh items differently and mix them with demographic and driving data to set prices.

For a practical look at how insurers translate risk into price, regulators and industry analysts often point to rate-setting methodologies; these explain why two carriers in the same ZIP code can quote dramatically different premiums. Learn more about how companies set rates and the factors they file with regulators via how insurers set insurance rates. This clarifies that insurance scoring is less about punishing people and more about statistical prediction—though the ethics and fairness of that approach remain debated.

Key insight: understanding the mechanics behind PolicyScore gives you leverage — you can change the inputs your insurer sees and reduce what you pay.

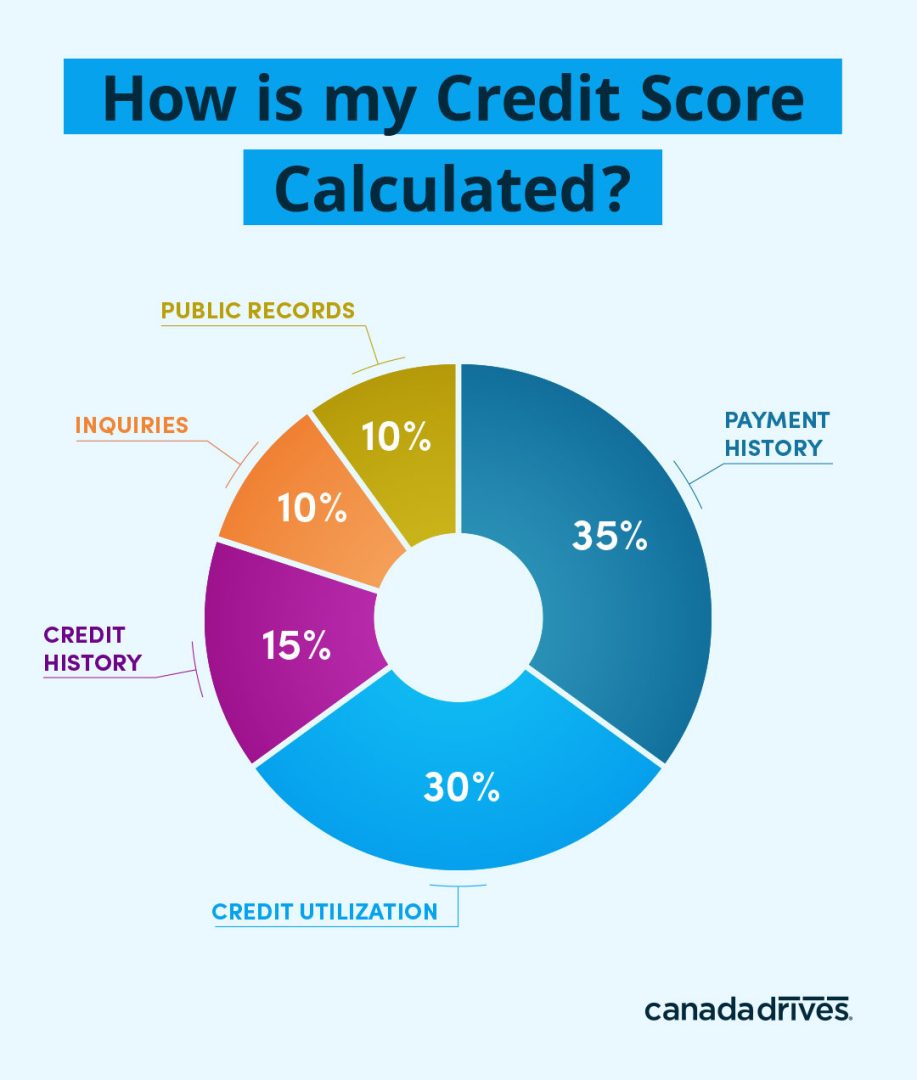

Which credit-report factors matter most in your PolicyScore?

Not all credit data is equal. The biggest contributors to most credit-based insurance scores are payment history and credit utilization. Late payments and high balances tend to push scores down, which insurers interpret as a higher likelihood of claims.

Other inputs include the length of credit history, the mix of credit (installment vs revolving), and recent hard inquiries. Thin files or no credit history can also produce higher quotes because the model has less data to reward low-risk behavior. Different carriers give different weight to these items—State Farm and Progressive, for example, can treat the same file quite differently—so shopping matters.

Key insight: focus first on consistent on-time payments and lowering utilization—those moves yield the biggest improvements in ScoreShield-style models.

Why your location and state rules change how credit impacts your premium

State regulation shapes how much credit matters. Some states restrict or ban the use of credit in rate-setting, while others allow broad use. That’s why Alexis saw much higher quotes in Florida than she might in California or Massachusetts, where restrictions reduce or eliminate credit’s role.

Insurers file models with state regulators, and differences between filings explain geographic variability. For a practical list of savings tactics tied to your policy choices (bundles, discounts, telematics), check guides on available discounts: auto insurance discounts explained. Geographic differences mean you should compare offers across carriers and ask precise questions about how much weight they give to your credit profile.

Key insight: never assume your current insurer’s quote is the market norm—shopping in different ZIP codes and carriers can expose large gaps that come from how credit is used locally.

Practical steps to improve your CreditGuard and lower premiums

Start by pulling your credit reports from the major bureaus and scanning for errors. Disputing inaccuracies often yields quick wins and is a free step toward a better InsureScorePro. Next, prioritize on-time payments: automation or calendar reminders reduce late-pay incidents that insurers penalize.

Work on your credit utilization by paying down card balances and keeping utilization under roughly 30%. Avoid multiple hard inquiries in a short window—timing applications for when it truly matters avoids unnecessary dinging. If your file is thin, opening and maintaining a small revolving account can lengthen your history and diversify your mix, which ScoreSense-type algorithms may reward.

For complex situations—major medical bills, bankruptcy, or identity theft—consider a certified credit counselor; programs under names like CreditCare and CreditScoreBoost offer structured plans. Finally, document improvements and re-shop after your score moves; even moderate gains can unlock PremiumProtect-level savings.

Key insight: credit repair is cumulative—small, consistent steps compound into meaningful insurance savings over months, not days.

Other ways to reduce premiums while you improve your score

If changing your credit takes time, use complementary levers to lower premiums now. Bundling auto and home policies with the same carrier often triggers discounts, and raising deductibles reduces annual cost if you can afford the larger out-of-pocket in a claim.

Maintaining a clean driving record, installing approved safety devices, and enrolling in telematics programs or defensive driving courses are immediate ways to lower rates. Many insurers list these savings under their underwriting guides; for tips on maximizing discounts based on your policy choices, review practical discount guides like the one covering auto insurance discounts and rate strategies such as insurance rate-setting basics. Combining these with credit improvements gives the best chance to beat stubborn quotes.

Key insight: treat credit improvement and traditional discounts as complementary strategies—together they shorten the path to affordable coverage.