En bref — Riders let you tailor a life policy without buying separate contracts. Think of add-ons like PolicyPlus or RiderFlex that plug real gaps: early access to benefits, premium waivers on disability, and modest coverage for children or spouses. Compare costs versus existing workplace benefits, check exclusions and waiting periods, and lock in key riders at purchase for best pricing. Use resources like the insurance beginner’s guide to start, and get a quote through smart tools when you’re ready.

Why this matters now: with families juggling mortgages, caregiving and volatile careers, a standard policy often isn’t enough. Riders transform that core protection into a living safety net — small premium additions can prevent catastrophic financial stress. Below, follow Alex and Ben’s journey as they build a tailored policy using riders such as LifeGuard Riders and FlexiCoverage, and learn when each add-on truly earns its keep.

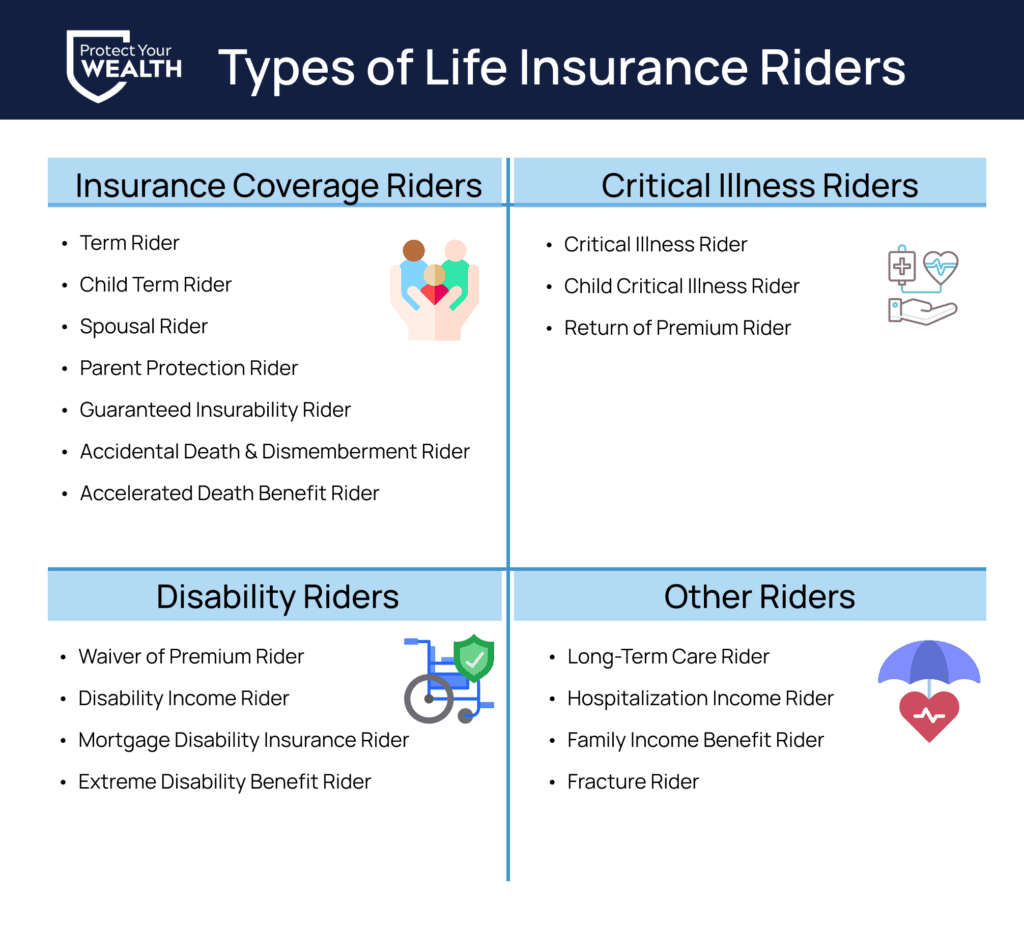

What are life insurance riders and how they customize your coverage

Think of a base life policy as the foundation of a house and riders as the rooms and systems you add later. A rider is an optional bolt-on that changes when or how benefits are paid — not a separate contract. For Alex and Ben, adding a Critical Illness rider meant they could tap cash if a serious diagnosis hit, avoiding the need to drain savings while they recovered.

Riders like BenefitBoost or RiderEnhance can be included at purchase or, sometimes, later — though initial application gives better pricing and more options. If you want a primer on core policies before customizing, read this clear overview on how insurance policies work. Key insight: riders make a policy flexible without the complexity of multiple standalone products.

Core differences: policy vs rider

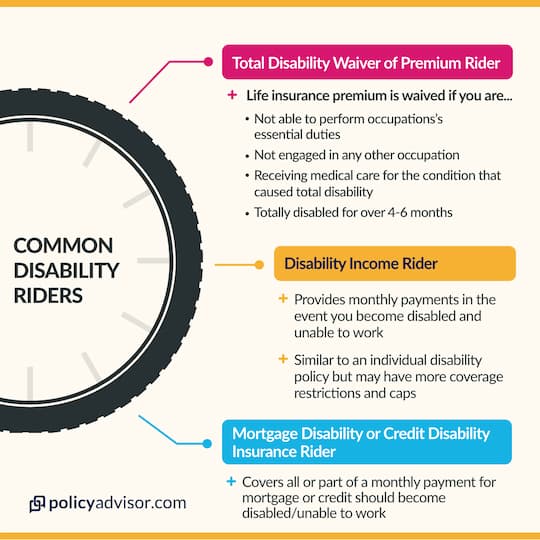

The main policy is the fundamental death benefit; a rider is a targeted add-on that addresses a specific risk like disability or a major illness. For Alex and Ben, the base policy covered their mortgage, while a Waiver of Premium rider insured the policy would stay active if one of them became disabled and couldn’t work.

PolicyAdvantagestyle= » »> and CoverageExpand style add-ons are examples of how insurers package common protections. Important to remember: riders usually raise premiums, but they often cost far less than buying separate long-term care or disability policies outright. Insight: riders are cost-effective gap-fillers when chosen strategically.

Popular riders explained: which ones people actually use

Here are the riders clients ask about most, presented with what they do and who benefits. Alex added an Accelerated Death Benefit so they could access part of the death benefit if a terminal diagnosis occurred; this avoided selling investments during a crisis.

If you want a step-by-step on tailoring coverage, this article on customizing insurance coverage explains trade-offs and pricing. The bottom line: pick riders that cover realistic, expensive risks your household faces.

Watching a short explainer helped Alex and Ben decide between an employer disability plan and adding a Waiver of Premium or RiderFlex option to their personal policy. Key takeaway: visual guides clarify exclusions and waiting periods that matter most at claim time.

Living benefits: support while you’re still alive

Some riders are “living benefits” — they pay out during the insured’s lifetime for qualifying events. The most common: the Accelerated Death Benefit, the Critical Illness rider, and income-protection options tied to disability.

For households where income equals security, a rider that protects monthly cash flow is invaluable. If disability insurance is on your radar, compare with dedicated products in this piece on disability insurance and income protection. Final insight: choose living-benefit riders when a short-term payout prevents long-term financial damage.

Alex and Ben used a video case study to see how a critical illness payout could cover childcare and home modifications. Concrete examples make the payout scenarios tangible and help decide if the extra premium is worth it. Ending thought: visualize how a rider payment would be used before committing to it.

Family-focused riders: keeping loved ones covered

Riders like Child Term Rider and Spouse Term Rider let you consolidate family coverage under one plan. Alex added a child rider after their baby arrived because it provided inexpensive, immediate coverage without separate underwriting.

Before adding family riders, check whether your partner can qualify for independent coverage at a similar cost; sometimes separate policies are cheaper or offer better long-term options. For renters or younger buyers balancing budget and protection, refer to practical tips in this guide on renters and protection choices. Insight: family riders are convenient, but compare prices and portability.

Cost, timing and underwriting — the practical steps to add a rider

The best moment to add riders is when you buy the policy. Insurers offer the widest menu and better rates then. If you delay, you may face new medical questions or restrictions, and fewer options to choose from.

Steps Alex and Ben followed: assess needs, consult an advisor, complete underwriting, then read the fine print. For those who prefer starting with numbers, this tool for smart insurance quotes speeds up budgeting. Final tip: always read exclusions and waiting periods — that’s where surprises hide.

When a rider isn’t worth it: avoid overbuying

Not every add-on is smart. If you already have solid employer disability coverage, don’t duplicate protection. Alex discovered their workplace plan covered short-term disability, so they skipped redundant riders and used the savings to boost emergency funds instead.

For insights on overlapping protections and tax implications, this resource on insurance and taxes helps you weigh net benefits. Remember: a rider should solve a real, plausible financial gap — otherwise it’s just another bill. Closing thought: match riders to real needs, not fears.

Choosing names that sell: branding and real value

Insurers market riders with catchy names like LifeChoice Riders, SecureOption, or PolicyPlus. The label can help you recognize product intent, but focus on the mechanics: triggers, payout amounts, and exclusions.

Brands such as LifeGuard Riders or CoverageExpand promise flexibility, while packages like FlexiCoverage and SecureOption emphasize adaptability. Rule of thumb: read the fine print behind the branding to see if the promise holds. Final insight: marketing names are useful shortcuts — but the contract controls the outcome.

Next steps: practical checklist to decide on riders

Start with a snapshot of your finances: mortgage, dependents, emergency savings and employer benefits. Then ask whether a rider addresses a plausible, high-cost event that would otherwise cause long-term harm.

For a broader view of long-term care options as an alternative to some riders, see this overview of long-term care insurance. Last point: prioritize riders that preserve liquidity and income — those choices usually deliver the most immediate value.