Denied a claim? That hit-you-in-the-gut moment is more common than you think, and it doesn’t have to be the end of the road. In this piece we follow Maya, a policyholder who gets a denied medical claim, to show you how denials happen, what to do first, and how to build an appeal that actually gets results. You’ll learn how to read the insurer’s notice, assemble the right paperwork—from a knockout Letter of Medical Necessity to a chronological timeline of treatment—and when to push from an internal appeal to an external review. Along the way we’ll point out signs of stalling or bad faith, explain how HIPAA gives you access to records, and show when to bring in pros like a public adjuster or attorney to tilt the odds in your favor. Tools and services with names like ClaimShield, AppealWise and ClaimResolve are mentioned so you know what to ask for when you call for help. Stick with Maya’s story and you’ll finish with a clear playbook to turn that “no” into a “yes.”

En bref — key takeaways you should keep front of mind: Read the denial letter first; fix admin errors fast; get a detailed Letter of Medical Necessity; compile a timeline and full records under HIPAA; file the internal appeal before the deadline; escalate to an external review when needed; call a pro (public adjuster or lawyer) if the insurer stonewalls. These moves turn a simple denial into an actionable challenge.

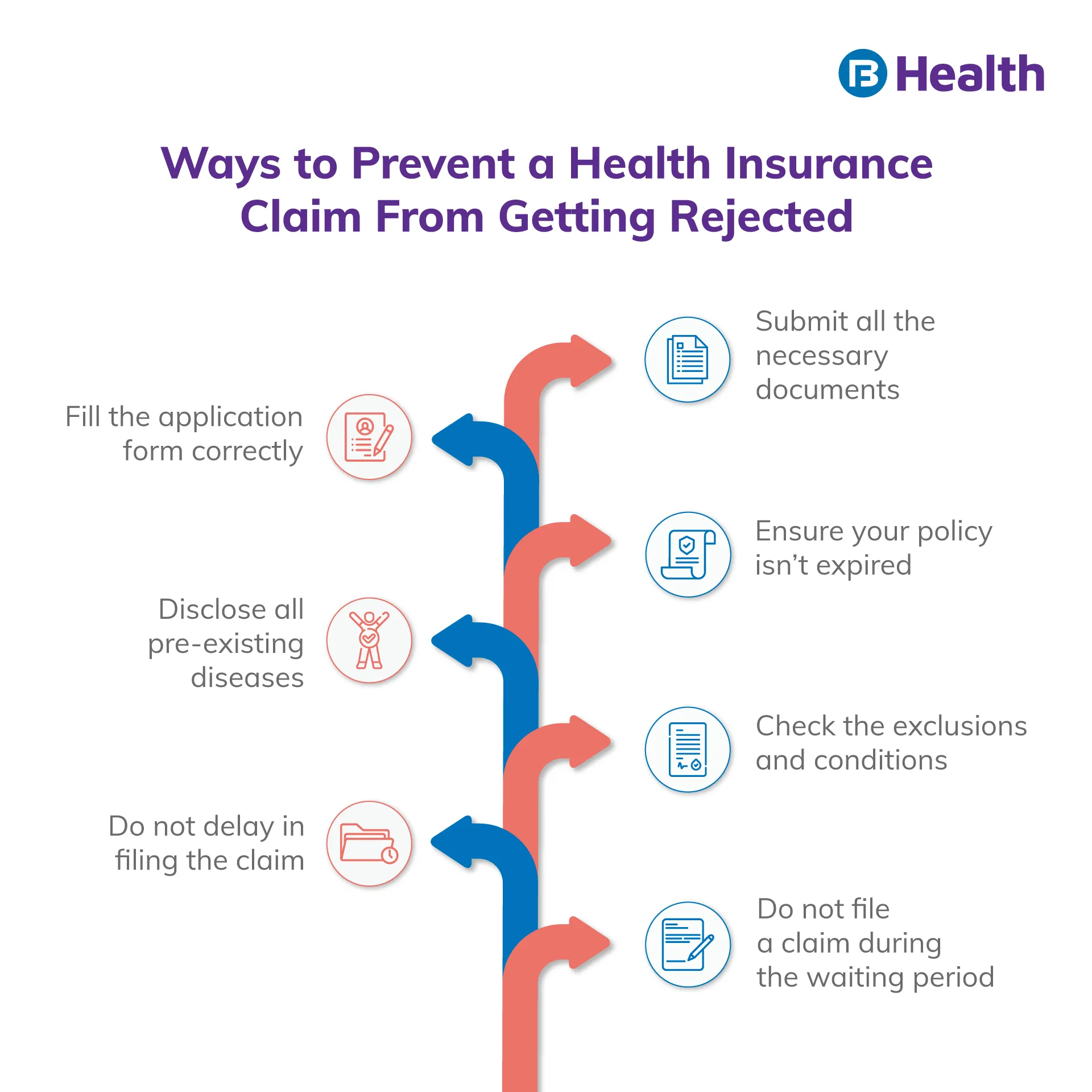

Why insurers deny claims and how to read the denial notice

When Maya first opened her denial, the insurer’s letter felt deliberately opaque. But every denial must state a reason—usually in an Explanation of Benefits (EOB)—and that reason is your target. Typical causes include not medically necessary, not a covered benefit, pre-existing condition, out-of-network, incorrect coding, or missing prior authorization.

Start by circling the insurer’s stated reason and the appeal deadline; treat the deadline like the single most important fact in the letter. From there, decide whether this is an administrative fix (misspelling, wrong code) or a medical-policy fight that needs clinical proof.

Common denial reasons and the immediate moves that win

Administrative errors: These are the easiest fixes—wrong name, missing DOB, bad billing code. Maya’s provider corrected a code and resubmitted within 48 hours and the claim was paid. If it’s an admin error, ask the provider to refile immediately; don’t start a formal appeal yet.

Lack of medical necessity: Here the insurer says the treatment isn’t essential. Your counter is a detailed Letter of Medical Necessity and supporting records showing prior treatments tried and failed, exactly what Maya’s physician provided. That letter should name the diagnosis, explain why other options won’t work, and spell out risks of withholding care.

Prior authorization or network issues: These can be tricky—sometimes the provider believed they had authorization but didn’t. Track down the authorization log, request internal office notes, and if the provider was at fault, ask them to take responsibility for the resubmission or to provide an appeal-ready statement.

Key insight: Every denial has a reason you can attack. Identify whether it’s a paperwork problem or a policy interpretation, then assemble evidence that addresses that exact reason.

Gather evidence like a pro: records, timelines, and the Letter of Medical Necessity

Once Maya knew the denial reason, she used HIPAA rights to request a complete medical record set from her clinic. HIPAA lets you obtain all treating notes, test results, and prior authorization correspondence—these are the documents that turn assertions into facts.

Build a chronological file: intake notes, diagnostic tests, conservative treatments tried and failed, the decision to escalate, and the exact treatment recommended. Highlight key phrases and tie them to policy language when possible. A clear timeline helped Maya show that the recommended care was the medically logical next step.

Don’t forget extra proof: photos for property claims, contractor estimates, receipts for out-of-pocket costs, or a second specialist opinion. For practical filing guidance, see this how to file an insurance claim and this step-by-step claim filing guide for templates and evidence checklists.

Tools & services: Platforms such as ClaimHelp, AppealSupport and AppealWise can streamline document collection and format a persuasive evidence packet for your internal appeal.

Key insight: A chronological, fully documented file leaves no wiggle room for the insurer’s reviewer—make the full story impossible to ignore.

Writing an appeal letter that actually compels a reviewer

Your appeal letter is a focused, factual brief—not an emotional plea. Maya’s letter opened with: name, policy number, claim number, denial date, and a one-sentence request to reverse the denial. Then she summarized the facts in chronological order and directly rebutted the insurer’s reason using quotes from policy sections and attached records.

Structure it: short opening, factual background, point-by-point rebuttal (quote the insurer’s denial language and counter it with exact evidence), list of attachments, and a clear closing demand for reversal and payment. Send it by certified mail or tracked delivery and note the submission date in your log.

Pro tip: Reference policy language when possible; if the insurer cites an exclusion, quote it and explain why your situation is outside that exclusion. For more on policy basics, check this insurance for beginners resource and review common pitfalls at common causes that void coverage.

Key insight: A concise, evidence-linked appeal that mirrors the insurer’s language is far more persuasive than a long, emotional narrative.

Deadlines, internal appeals, and the power of external review

Start with an internal appeal: follow the insurer’s instructions to the letter and file before the deadline—they often give 30–180 days depending on the plan. Maya filed within 20 days, included every record, and requested expedited review when her doctor certified urgency.

If the internal appeal fails, request an external review. This sends your case to an Independent Review Organization (IRO) with no financial ties to the insurer. Their decision is binding, and many overturned denials happen at this stage—don’t skip it. Your insurer must include instructions for this step in the final denial notice.

If the insurer drags its feet, ask your state Department of Insurance to intervene. Filing a complaint often prompts a faster, more reasonable company response because nobody wants regulator attention. For practical appeal checklists and timelines, this simple health insurance tips page is a helpful companion as you track documents and dates.

Key insight: Deadlines matter more than anything—missing one can lose your right to a review, so calendar everything and send proofs of delivery.

When to bring in outside help: public adjusters, attorneys, and escalation

Maya started alone but brought in a public adjuster after the insurer stonewalled on coverage for a high-cost therapy. Public adjusters work for you and are especially effective on property claims; they document loss value, negotiate, and often secure substantially better settlements. Similarly, an attorney is the right next step when you suspect bad faith or face a very large, complex denial.

Look for professionals who advertise services you recognize—names like ClaimResolve, DenyDefense, AppealPro, and InsureGuard are examples of the sort of specialized help available. If you prefer to try self-help first, use the online guides above to format your submissions and understand common insurer tactics.

Key insight: Bring in paid help when the cost/benefit favors you—pros convert denials into payouts much more efficiently than most consumers alone.

Signals that you should escalate to regulators or litigation

If the insurer keeps changing reasons, refuses to provide the full claim file, or misses statutory deadlines, those are red flags. Maya noticed shifting excuses and filed a complaint with her state DOI; the complaint forced the insurer to produce internal review notes and ultimately led to a quicker settlement.

Documentation of stalling, contradictory denial reasons, or failure to follow your policy’s appeal rules all strengthen a regulator complaint or a bad-faith lawsuit. Keep a call log, save every email, and keep copies of every submission. Those logs were central to Maya’s success when she escalated her case.

Key insight: Regulators act as effective referees—use the Department of Insurance when the insurer’s behavior looks like a pattern of evasive tactics.

Final practical checklist before you submit an appeal

Make sure your packet contains: identifying info and claim numbers, the denial letter, a clear appeal letter, chronological medical or damage records, a Letter of Medical Necessity (if applicable), prior authorization records (or explanation), receipts, photos, and a list of enclosed documents. Highlight key phrases and policy citations so the reviewer can scan and see the connection you’re making.

If you want a walkthrough on how to assemble these documents, start with this guide on how to file an insurance claim and pair it with the basics from insurance for beginners to make sure nothing gets missed.

Key insight: A single, complete, clearly organized appeal packet increases the likelihood your denial will be reversed—organization communicates credibility.