Flood insurance: why it matters now — Flooding ranks among the most frequent and costly natural disasters, and in recent years more unpredictable weather has pushed flood risk into places people thought were safe. Take Maya, a graphic designer in a coastal suburb who assumed her standard homeowner policy would cover everything; after a sudden storm surge in early 2025 she learned the hard way that standard homeowners insurance rarely covers flood damage. For property owners, that gap can mean facing repairs that run into the tens of thousands. This piece lays out the practical reasons to buy flood cover, how policies differ, and the concrete steps Maya (and you) can take to reduce premiums and get the right protection. We look at both the federally backed options and the growing private market, compare what gets paid for structural versus contents losses, and show how mitigation choices—like elevating utilities or adding flood vents—translate into lower costs. Along the way, you’ll meet familiar product names from the market and get pointers on where to find quotes, how insurers price risk, and which policy features matter most if you want true financial resilience.

En bref: Floods can hit outside mapped high-risk zones; one inch of water can cause major damage; mortgages in special flood hazard areas often require coverage; NFIP offers baseline protection while private carriers extend limits and options; simple mitigation lowers premiums over time.

Why flood insurance is essential in high-risk areas and beyond

Regulators and lenders treat flood risk seriously because catastrophic losses escalate quickly. If your home sits in a FEMA-designated high-risk zone and your mortgage is federally regulated, you’re typically required to carry flood insurance. That’s what happened to Maya: when her lender reviewed elevation certificates, adding a compliant policy became mandatory.

Even outside those zones, floods are common. FEMA has consistently shown a substantial portion of claims come from unexpected areas, and in 2025 that trend continued as urban runoff and stronger storms increased local flooding events. The clear message: risk is widespread and often underestimated.

For readers wondering whether a policy is worth it, remember: repairs add up fast. Insurers track losses showing that minimal water depths can damage mechanical systems, flooring and appliances—costs that often exceed emergency savings. This reality drives the practical need for protection beyond hope and DIY fixes.

Building vs contents: what a flood policy actually pays for

Flood insurance typically splits into two buckets: building coverage for the structure and systems, and contents coverage for personal belongings. Building coverage handles things like foundation walls, electrical and plumbing systems, and built-in fixtures. Contents coverage protects furniture, electronics and clothing up to policy limits.

Many homeowners are surprised that mold, gradual moisture damage, and some types of temporary living expenses aren’t universally covered—details vary between the federal National Flood Insurance Program (NFIP) and private carriers. That’s why comparing offerings matters: some private policies, including options from niche providers like FloodGuard or AquaShield Insurance, add endorsements for broader living-expense protection.

Example: Maya replaced carpet and two HVAC units after a flood. Her NFIP claim covered the primary structural repairs but not all replacement costs for high-end electronics; a private supplement would have narrowed the gap. The insight: matching coverage to your possessions prevents nasty surprises at claim time.

How to get the right flood coverage in 2025: steps that work

Start by checking your property’s flood designation and elevation. FEMA’s maps are the baseline, but local assessments and recent storm histories matter too. Once you know your exposure, evaluate the two main routes: the NFIP for standardized, federally backed policies, or private carriers for higher limits and customizable features.

Work with an agent who understands flood-specific underwriting and can show side-by-side comparisons. You can learn the basics with an insurance beginner’s guide, then move to tools that help you compare smart insurance quotes. If your property has unique features, consider how to customize your coverage so items like finished basements or detached garages are handled correctly.

Remember the waiting period: NFIP policies usually have a 30-day window before coverage begins, so purchase proactively. For Maya, starting that purchase well before hurricane season made filing a claim faster and less stressful when the storm hit.

Practical takeaway: get a tailored quote early and confirm what both building and contents cover so there are no coverage gaps when you need help.

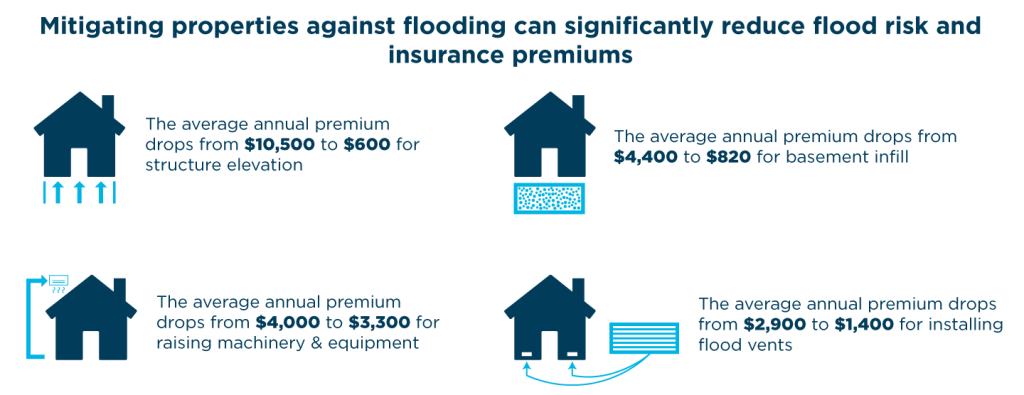

How homeowners lower premiums and an on-the-ground case study

Mitigation reduces both risk and cost. Elevating utilities above base flood elevation, installing flood vents, and improving yard drainage are concrete upgrades that insurers reward. Choosing a higher deductible lowers premiums too, but you should balance that against your ability to pay an out-of-pocket amount after a loss.

Consider Maya’s retrofit: she raised her furnace and electrical panel, added flood-resistant materials in the lower levels, and documented those changes for her insurer. The result was a measurable premium drop and faster claim processing because she had clear records. To understand pricing drivers, review resources on factors that affect premiums and how insurers set rates at insurance rate-setting.

Private market names can be part of the solution. Products such as RiskSafe Flood Cover, FloodSecure, FloodProtect Solutions, SafeHarbor Flood Insurance, FloodSure Coverage, WaterGuard Insurance, FloodRisk Shield, and FloodSmart Insurance illustrate the variety available—some focus on broader limits, others on rapid claims service or bundled home protection.

Bottom-line insight: targeted mitigation plus the right policy type can cut risk and reduce long-term cost exposure.

When to consider private flood insurance instead of just NFIP

If your property has high replacement costs or you want added perks—like coverage for additional living expenses—private policies may fill gaps left by NFIP. Private carriers often offer higher limits and optional endorsements for valuables or business interruption tied to home-based work.

For small business owners working from home, check resources on business assets coverage and home insurance protection to see where flood coverage fits with occupational risks. Maya, who freelances, included equipment replacement limits in her private-policy quote to avoid a work interruption after water damage.

Choosing between NFIP and private options is a balance of cost, coverage limits, and service expectations. A clear review of policy language and real-life claim examples will point you to the right fit. Decide with a full inventory and documented mitigation steps to strengthen both coverage and claims outcomes.

Final planning note before storms arrive

Don’t wait for weather warnings—flood insurance needs time to take effect and mitigation needs planning. Keep receipts and photos of upgrades, maintain an up-to-date inventory of belongings, and review renewal terms yearly so coverage keeps pace with property value and local flood dynamics.

If you want to dig deeper into broader disaster options or debunk myths about coverage, useful reads include natural disaster insurance options and common insurance myths debunked. Those guides will help you avoid the typical missteps people make when shopping for flood protection.

Closing insight for homeowners: proactive planning, documented mitigation, and the right mix of NFIP or private cover are what turn flood risk into manageable, insurable events.