Insurance and taxes intersect in ways most policyholders only notice when cash hits or leaves their accounts. In 2025 the rules are familiar but with enough nuance to surprise: whether a benefit is taxable often hinges on who paid the premiums, how a product is structured, and where you live. This article walks through the practical tax implications for disability, life, long‑term care and health insurance, highlights hidden charges on premium bills, and shows simple planning moves that can save real money.

We follow Alex, a 38‑year‑old project manager, and Maya, a small business owner, to illustrate decisions you can act on today. Along the way you’ll see how common products from hypothetical providers like InsureWise or PolicyPlus behave for taxes, and what questions to bring to your tax pro so insurance doesn’t become an accidental tax bill.

En bref: Premiums paid pre‑tax usually make benefits taxable. Death benefits are generally income tax‑free. Cash‑value access can trigger taxes or penalties if mishandled. Long‑term care contracts and health accounts offer specific deductions and deferrals. State premium taxes and assessments are often embedded in your bill. Smart planning—ownership, premium source, and product choice—reduces surprises.

How taxation shapes everyday insurance choices for policyholders

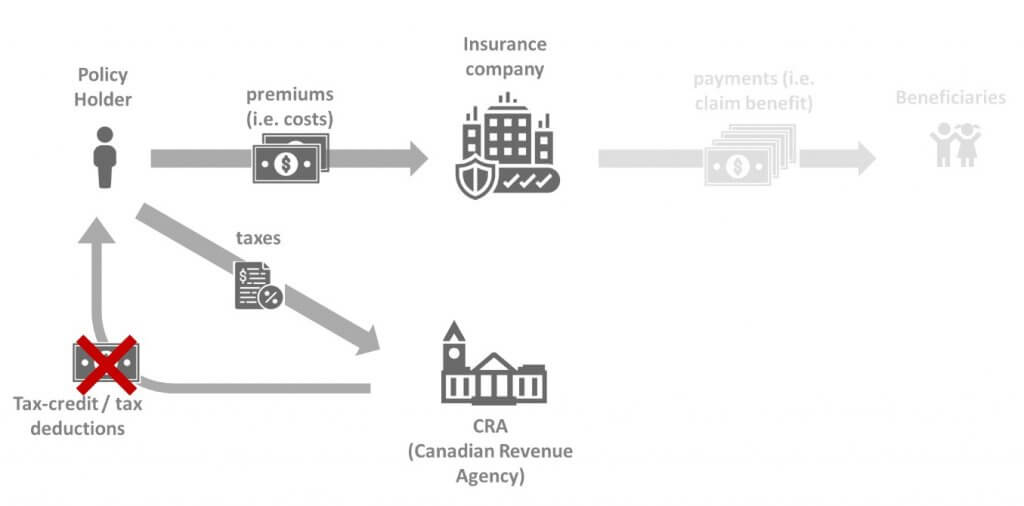

Start with the key rule: who pays the premium usually determines whether benefits are taxable. If an employer pays with pre‑tax dollars, benefits like disability income are often taxable when paid out. If you bought coverage yourself with after‑tax money, benefits are commonly tax‑free.

Alex learned this the hard way: his employer covered a group disability policy, and when he filed a claim the benefits were taxable, shrinking his net monthly recovery. That was avoidable—a supplemental individual policy from InsureWise purchased with after‑tax dollars would have produced tax‑free benefits and preserved more of his paycheck while disabled.

Key insight: check the premium payer before you assume benefits are tax‑free.

Disability insurance — employer vs individual vs government programs

Disability benefits fall into four practical buckets: employer‑sponsored plans, individual policies, Social Security disability, and VA disability. Each follows different tax rules tied to premium sourcing and other income.

If your employer pays the premium or you pay with pre‑tax dollars, plan benefits are normally taxed as income. If you pay the premium with after‑tax dollars, benefits are usually tax‑free. For Social Security disability some benefits become taxable when combined income passes IRS thresholds, while VA disability compensation remains income‑tax free.

Maya, the small business owner, kept an individually owned policy from PolicyShield to top up group coverage because it would pay tax‑free when she needed it—she intentionally used after‑tax dollars to secure that protection.

Key insight: supplement employer plans with individually‑owned coverage if you want tax‑free disability benefits.

Life insurance — what’s taxed, what’s not, and traps with cash value

Life insurance proceeds paid at death are typically income tax‑free to beneficiaries, which is why life policies remain a popular estate planning tool. But when policies build cash value, withdrawals, loans, and surrenders introduce tax complexity that matters long before death.

Withdrawals up to your basis (what you paid in premiums) are generally tax‑free unless the policy is a modified endowment contract (MEC). Loans against a non‑MEC policy are usually tax‑free while the policy remains in force, but surrendering with an outstanding loan can create taxable gain. MECs carry less favorable tax treatment and possible penalties before age 59½.

In a practical tweak, Alex used a policy from PolicyPlus to accumulate cash value for business‑cycle needs, but he avoided taking taxable withdrawals by using policy loans strategically and monitoring the policy’s status to prevent a taxable lapse.

Key insight: if you rely on life‑insurance cash value, document basis, avoid MEC classification unless intentional, and treat loans carefully.

Health care and long‑term care: deductions, credits and the real limits

Health premiums are deductible in specific situations. Employer‑paid group premiums paid pre‑tax are not deductible by the employee, while self‑employed individuals can often deduct eligible health insurance premiums directly against income. Itemizing allows unreimbursed medical expenses to be deductible to the extent they exceed 7.5% of adjusted gross income.

Qualified long‑term care (LTC) insurance benefits are generally tax‑free if the contract meets IRS rules (no cash surrender value and guaranteed renewable). Premiums for qualified LTC insurance may be deductible as medical expenses but are subject to age‑based caps. For the 2025 tax year those deductible limits include $480 for age 40 or younger, $900 for 41–50, $1,800 for 51–60, $4,810 for 61–70, and $6,020 for 71+.

Maya used a combination of TaxSaver Insurance LTC riders and a high‑deductible health plan with an HSA to stack tax advantages: HSA contributions reduced taxable income, while LTC premiums counted toward itemized medical deductions within IRS limits.

Key insight: combine HSAs, qualified LTC contracts, and careful itemizing to maximize tax efficiency for health‑related coverage.

Premium taxes, hidden fees and why your bill looks higher than you thought

Beyond federal income rules, your premium often carries embedded state and local charges. premium taxes, guaranty fund assessments, stamp duties, and sometimes sales or excise taxes are typically passed through by insurers and increase the price you pay. Rates vary widely by state and line of business.

For example, two people with the same homeowner policy in different states may pay materially different totals because one state applies a premium tax or an insurance‑specific levy. Businesses that buy surplus lines or international coverages may face additional fee filings or direct taxes.

When Alex compared quotes from ClaimSecure and SecureClaim, the sticker price looked similar, but ClaimSecure disclosed a state premium tax and a guaranty fund charge that made its effective cost higher; reading the policy bill uncovered that difference.

Key insight: ask insurers to break down premium components and factor state premium taxes into comparisons—sticker price isn’t the final cost.

Smart planning moves that cut tax drag on insurance

Good planning is about ownership, premium source, and product fit. Own key policies personally when you want tax‑free benefits; consider ILITs for estate exclusion; use HSAs and annuities for deferred growth; and for businesses, deduct ordinary and necessary insurance expenses while monitoring fringe benefits rules.

Small business owner Maya organized benefits so group health premiums stayed tax‑advantaged for employees, while the company purchased a business‑owned life policy for key person coverage; premiums were structured and documented to remain deductible where allowed. For corporate tax optimization, insurers and companies also consider tools like reinsurance and transfer pricing—areas where firms often consult firms such as TaxPolicy Partners or use vendors branding like TaxGuard and TaxSmart Insurance to model impacts.

Key insight: structure ownership and premium flows deliberately—these mechanics determine whether benefits are taxable or tax‑free.

What to watch next: regulatory and market shifts that matter in 2025

The regulatory environment is evolving: global initiatives on base erosion, increased IRS enforcement, and state changes to premium taxes can shift economics quickly. InsurTech and usage‑based products also challenge traditional tax collection points—think pay‑per‑mile auto insurance and micro‑policies where tax jurisdictions may struggle to keep pace.

Climate risk and catastrophic losses will continue to pressure premiums and could prompt new levies or relief programs. Watch for state‑level legislation that changes premium tax structures and for industry guidance from tax advisors and partners like SureTax Coverage as rules adapt.

Key insight: stay alert to state tax changes and product innovations—what’s tax‑efficient today may shift with new rules or new policy forms.